HMM Based Trading Applications

HMM Based Trading Applications

From Regime Detection to Profitable Trading Strategies

See the Notebook source on GitHub.

Your Journey So Far

Notebook 1: Why Use Log Returns?

You learned WHY log returns are necessary:

- Stationarity, additivity, scale invariance

- Mathematical properties required for HMMs

Notebook 2: HMM Basics

You learned HOW HMMs work:

- Hidden states, transition matrices, emissions

- Viterbi and forward-backward algorithms

Notebook 3: Hidden Regime Pipeline

You learned to DETECT regimes:

- Pipeline setup and execution

- Regime classification and duration

- Model selection and validation

Notebook 4: Trading Applications (This Notebook)

You’ll learn to TRADE using regimes:

- Risk management by regime

- Technical indicator integration

- Position sizing and signal generation

- Backtesting and validation

What This Notebook Covers

Part A: Regime-Specific Risk Analysis (Sections 1-2) Part B: Technical Indicator Integration (Sections 3-4) Part C: Portfolio Applications (Sections 5-6) Part D: Backtesting & Validation (Sections 7-8) Part E: Best Practices & Conclusion (Section 9)

Prerequisites

Before starting this notebook:

- ✓ Completed Notebook 03

- ✓ Understand regime detection pipeline

- ✓ Familiar with confidence levels and regime characteristics

Important: This notebook demonstrates trading concepts for educational purposes. Always backtest thoroughly and start with paper trading before risking real capital.

1import sys

2from pathlib import Path

3import numpy as np

4import pandas as pd

5import matplotlib.pyplot as plt

6import seaborn as sns

7from datetime import datetime, timedelta

8import warnings

9warnings.filterwarnings('ignore')

10

11# Add parent to path

12sys.path.insert(0, str(Path().absolute().parent))

13

14# Import hidden_regime

15import hidden_regime as hr

16

17# Plotting

18plt.style.use('seaborn-v0_8-whitegrid')

19sns.set_palette(sns.color_palette())

20

21print(f"Imports complete")

22print(f"hidden-regime version: {hr.__version__}")

Imports complete

hidden-regime version: 1.0.0

Setup: Run Pipeline from Notebook 03

We’ll reuse the same NVDA example to demonstrate trading applications.

1# Create pipeline (same as Notebook 03)

2ticker = 'NVDA'

3n_states = 3

4

5pipeline = hr.create_financial_pipeline(

6 ticker=ticker,

7 n_states=n_states,

8 include_report=False

9)

10

11# Execute pipeline

12report = pipeline.update()

13result = pipeline.component_outputs['analysis']

14raw_data = pipeline.data.get_all_data()

15

16print(f"Pipeline complete: {len(result)} days analyzed")

17print(f"Date range: {result.index[0].date()} to {result.index[-1].date()}")

Training on 500 observations (removed 0 NaN values)

Pipeline complete: 500 days analyzed

Date range: 2023-10-18 to 2025-10-15

Part A: Regime-Specific Risk Analysis

1. Risk Metrics by Regime

Different regimes have different risk characteristics. Understanding these helps with:

- Position sizing: Larger positions in low-risk regimes

- Stop-loss placement: Wider stops in high-volatility regimes

- Strategy selection: Trend-following vs mean-reversion

Key Risk Metrics

Value at Risk (VaR): Maximum expected loss at confidence level $\alpha$

$ \text{VaR}_\alpha = -F^{-1}(\alpha) $

where $F^{-1}$ is the inverse CDF of returns.

Expected Shortfall (ES): Average loss beyond VaR

$ \text{ES}_\alpha = E[r \mid r \leq -\text{VaR}_\alpha] $

Sharpe Ratio: Risk-adjusted return

$ \text{Sharpe} = \frac{\mu - r_f}{\sigma} $

where $\mu$ is mean return, $r_f$ is risk-free rate, $\sigma$ is volatility.

Maximum Drawdown: Largest peak-to-trough decline

$ \text{MDD} = \max_{t} \left[ \frac{\max_{\tau \leq t} P_\tau - P_t}{\max_{\tau \leq t} P_\tau} \right] $

1# Get log returns aligned with regimes

2log_return_col = next((col for col in raw_data.columns if col.lower() == 'log_return'), None)

3

4if log_return_col is None:

5 raise ValueError("Could not find log_return column")

6

7# Calculate comprehensive risk metrics by regime

8risk_metrics = {}

9

10for regime in sorted(result['regime_name'].unique()):

11 regime_data = result[result['regime_name'] == regime]

12 regime_indices = regime_data.index

13 regime_returns = raw_data.loc[regime_indices, log_return_col].dropna()

14

15 if len(regime_returns) < 2:

16 continue

17

18 # Basic statistics

19 mean_daily = regime_returns.mean()

20 std_daily = regime_returns.std()

21 mean_annual = mean_daily * 252

22 std_annual = std_daily * np.sqrt(252)

23

24 # Sharpe ratio (assuming 0% risk-free rate)

25 sharpe = (mean_annual / std_annual) if std_annual > 0 else 0

26

27 # Maximum drawdown

28 cumulative = (1 + regime_returns).cumprod()

29 running_max = cumulative.expanding().max()

30 drawdown = (cumulative - running_max) / running_max

31 max_drawdown = drawdown.min()

32

33 # Value at Risk

34 var_95 = np.percentile(regime_returns, 5)

35 var_99 = np.percentile(regime_returns, 1)

36

37 # Expected Shortfall (Conditional VaR)

38 es_95 = regime_returns[regime_returns <= var_95].mean()

39 es_99 = regime_returns[regime_returns <= var_99].mean()

40

41 # Win rate and profit factor

42 wins = regime_returns[regime_returns > 0]

43 losses = regime_returns[regime_returns < 0]

44 win_rate = len(wins) / len(regime_returns) if len(regime_returns) > 0 else 0

45 total_wins = wins.sum() if len(wins) > 0 else 0

46 total_losses = abs(losses.sum()) if len(losses) > 0 else 0

47 profit_factor = total_wins / total_losses if total_losses > 0 else float('inf')

48

49 risk_metrics[regime] = {

50 'days': len(regime_returns),

51 'mean_daily': mean_daily * 100,

52 'std_daily': std_daily * 100,

53 'mean_annual': mean_annual * 100,

54 'std_annual': std_annual * 100,

55 'sharpe': sharpe,

56 'max_drawdown': max_drawdown * 100,

57 'var_95': var_95 * 100,

58 'var_99': var_99 * 100,

59 'es_95': es_95 * 100,

60 'es_99': es_99 * 100,

61 'win_rate': win_rate * 100,

62 'profit_factor': profit_factor

63 }

64

65# Display risk metrics table

66print("Risk Metrics by Regime")

67print("=" * 100)

68print(f"{'Regime':<12} {'Days':<8} {'Ann Return':<12} {'Ann Vol':<12} {'Sharpe':<10} {'Max DD':<12}")

69print("-" * 100)

70

71for regime in sorted(risk_metrics.keys()):

72 m = risk_metrics[regime]

73 print(f"{regime:<12} {m['days']:<8} {m['mean_annual']:>10.1f}% {m['std_annual']:>10.1f}% "

74 f"{m['sharpe']:>9.2f} {m['max_drawdown']:>10.1f}%")

75

76print("=" * 100)

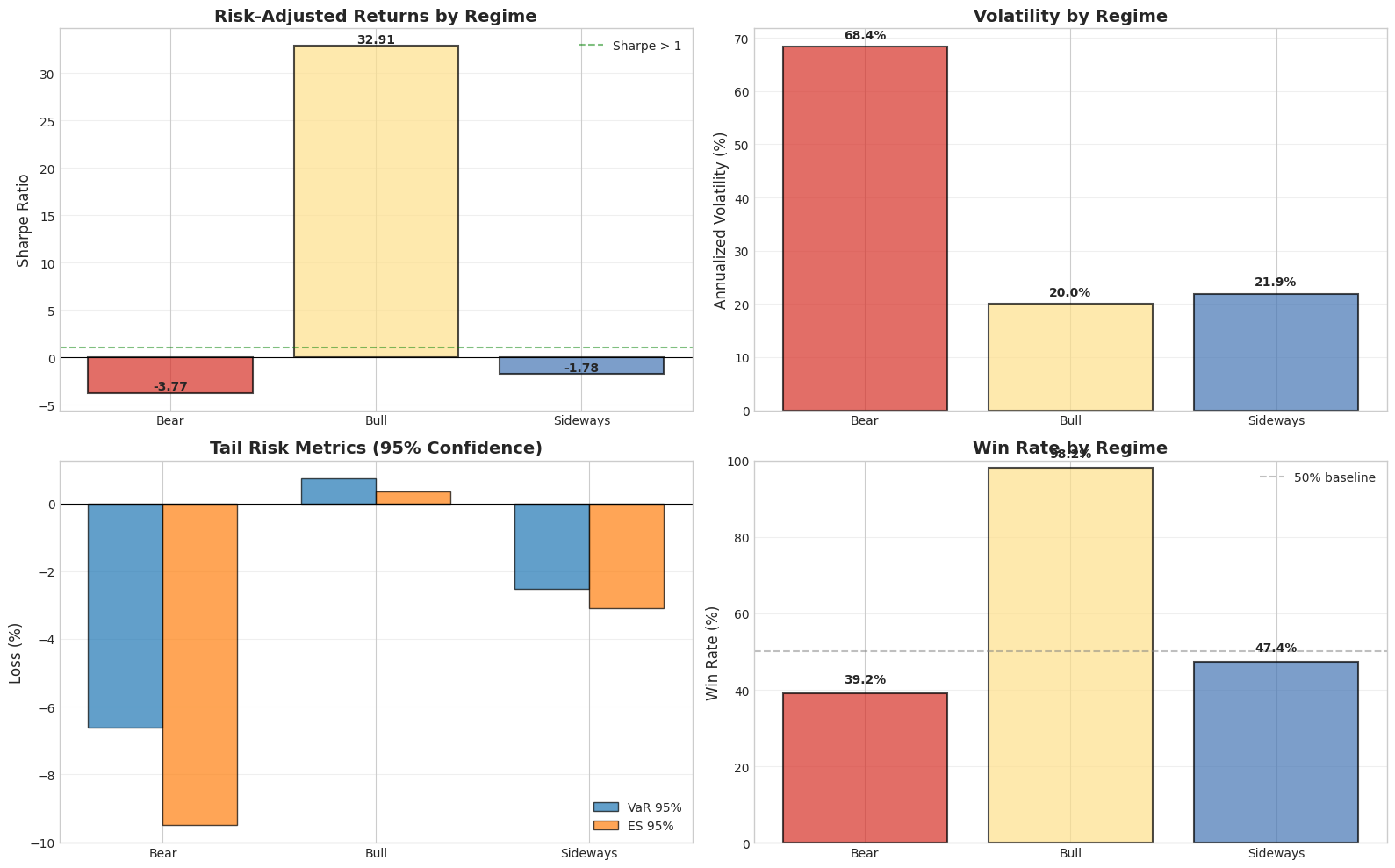

Risk Metrics by Regime

====================================================================================================

Regime Days Ann Return Ann Vol Sharpe Max DD

----------------------------------------------------------------------------------------------------

Bear 97 -258.0% 68.4% -3.77 -71.5%

Bull 110 657.7% 20.0% 32.91 -0.0%

Sideways 293 -39.1% 21.9% -1.78 -44.1%

====================================================================================================

1# Visualize risk metrics

2fig, axes = plt.subplots(2, 2, figsize=(16, 10))

3

4# Get regime colors

5from hidden_regime.visualization import get_regime_colors

6unique_regimes = sorted(risk_metrics.keys())

7color_list = get_regime_colors(len(unique_regimes), color_scheme="colorblind_safe")

8regime_colors = dict(zip(unique_regimes, color_list))

9

10# 1. Sharpe Ratio comparison

11ax = axes[0, 0]

12regimes = list(risk_metrics.keys())

13sharpes = [risk_metrics[r]['sharpe'] for r in regimes]

14colors = [regime_colors[r] for r in regimes]

15

16bars = ax.bar(regimes, sharpes, color=colors, alpha=0.7, edgecolor='black', linewidth=1.5)

17ax.axhline(y=0, color='black', linestyle='-', linewidth=0.8)

18ax.axhline(y=1, color='green', linestyle='--', alpha=0.5, label='Sharpe > 1')

19ax.set_ylabel('Sharpe Ratio', fontsize=12)

20ax.set_title('Risk-Adjusted Returns by Regime', fontsize=14, fontweight='bold')

21ax.grid(True, alpha=0.3, axis='y')

22ax.legend()

23

24# Add value labels

25for bar, val in zip(bars, sharpes):

26 height = bar.get_height()

27 ax.text(bar.get_x() + bar.get_width()/2, height + 0.05,

28 f'{val:.2f}', ha='center', va='bottom', fontweight='bold')

29

30# 2. Volatility comparison

31ax = axes[0, 1]

32vols = [risk_metrics[r]['std_annual'] for r in regimes]

33bars = ax.bar(regimes, vols, color=colors, alpha=0.7, edgecolor='black', linewidth=1.5)

34ax.set_ylabel('Annualized Volatility (%)', fontsize=12)

35ax.set_title('Volatility by Regime', fontsize=14, fontweight='bold')

36ax.grid(True, alpha=0.3, axis='y')

37

38for bar, val in zip(bars, vols):

39 height = bar.get_height()

40 ax.text(bar.get_x() + bar.get_width()/2, height + 1,

41 f'{val:.1f}%', ha='center', va='bottom', fontweight='bold')

42

43# 3. VaR and ES comparison

44ax = axes[1, 0]

45x = np.arange(len(regimes))

46width = 0.35

47

48var_95_vals = [risk_metrics[r]['var_95'] for r in regimes]

49es_95_vals = [risk_metrics[r]['es_95'] for r in regimes]

50

51ax.bar(x - width/2, var_95_vals, width, label='VaR 95%', alpha=0.7, edgecolor='black')

52ax.bar(x + width/2, es_95_vals, width, label='ES 95%', alpha=0.7, edgecolor='black')

53

54ax.set_ylabel('Loss (%)', fontsize=12)

55ax.set_title('Tail Risk Metrics (95% Confidence)', fontsize=14, fontweight='bold')

56ax.set_xticks(x)

57ax.set_xticklabels(regimes)

58ax.legend()

59ax.grid(True, alpha=0.3, axis='y')

60ax.axhline(y=0, color='black', linestyle='-', linewidth=0.8)

61

62# 4. Win rate and profit factor

63ax = axes[1, 1]

64win_rates = [risk_metrics[r]['win_rate'] for r in regimes]

65

66bars = ax.bar(regimes, win_rates, color=colors, alpha=0.7, edgecolor='black', linewidth=1.5)

67ax.axhline(y=50, color='gray', linestyle='--', alpha=0.5, label='50% baseline')

68ax.set_ylabel('Win Rate (%)', fontsize=12)

69ax.set_title('Win Rate by Regime', fontsize=14, fontweight='bold')

70ax.grid(True, alpha=0.3, axis='y')

71ax.legend()

72ax.set_ylim(0, 100)

73

74for bar, val in zip(bars, win_rates):

75 height = bar.get_height()

76 ax.text(bar.get_x() + bar.get_width()/2, height + 2,

77 f'{val:.1f}%', ha='center', va='bottom', fontweight='bold')

78

79plt.tight_layout()

80plt.show()

Interpretation & Trading Implications

Sharpe Ratio Analysis:

- Best regime: Highest Sharpe ratio → allocate more capital

- Sharpe > 1: Excellent risk-adjusted returns

- Sharpe < 0: Losing money on average → avoid or short

Volatility Management:

- High volatility regimes: Use wider stop-losses, smaller positions

- Low volatility regimes: Can use tighter stops, larger positions

- Position size ∝ $\frac{1}{\sigma}$ (inverse volatility scaling)

Tail Risk (VaR/ES):

- Expected Shortfall > VaR: Fat-tailed distribution, expect worse losses

- Use ES for position sizing: $\text{Position Size} = \frac{\text{Risk Budget}}{|ES|}$

Win Rate:

- High win rate: Many small wins (mean-reversion strategy)

- Low win rate: Few large wins (trend-following strategy)

- Combine with profit factor for complete picture"

2. Dynamic Position Sizing

Regime-Based Position Sizing Formula

Combine multiple risk factors to determine optimal position size:

$ \text{Position} = \text{Base} \times \underbrace{\frac{\sigma_{\text{target}}}{\sigma_{\text{regime}}}}_{\text{Vol Scaling}} \times \underbrace{\text{Confidence}}_{\text{Regime Certainty}} \times \underbrace{f(\text{Sharpe})}_{\text{Risk-Adjusted}} $

Where:

- Base: Standard position size (e.g., 100% for full allocation)

- Vol Scaling: Adjust for regime volatility

- Confidence: Current regime probability from HMM

- Risk-Adjusted: Additional scaling based on Sharpe ratio

Implementation Strategy

- Set target volatility: $\sigma_{\text{target}} = 15\%$ (annual)

- Scale by regime volatility: Position $\propto \frac{1}{\sigma_{\text{regime}}}$

- Apply confidence filter: Reduce positions when confidence < 70%

- Apply regime quality filter: Reduce positions in negative Sharpe regimes

1# Calculate position sizing for each day

2target_vol = 15.0 # Target 15% annualized volatility

3position_sizes = []

4

5for idx in result.index:

6 current_regime = result.loc[idx, 'regime_name']

7 confidence = result.loc[idx, 'confidence']

8

9 # Get regime metrics

10 regime_vol = risk_metrics[current_regime]['std_annual']

11 regime_sharpe = risk_metrics[current_regime]['sharpe']

12

13 # Base position (100% = full allocation)

14 base_position = 1.0

15

16 # Volatility scaling

17 vol_scalar = target_vol / regime_vol if regime_vol > 0 else 0

18 vol_scalar = min(vol_scalar, 2.0) # Cap at 2x leverage

19

20 # Confidence scaling

21 conf_scalar = confidence if confidence > 0.6 else confidence * 0.5 # Penalize low confidence

22

23 # Sharpe-based scaling

24 if regime_sharpe > 1.0:

25 sharpe_scalar = 1.0 # Full position

26 elif regime_sharpe > 0.5:

27 sharpe_scalar = 0.75 # Reduce position

28 elif regime_sharpe > 0:

29 sharpe_scalar = 0.5 # Half position

30 else:

31 sharpe_scalar = 0.0 # No position in negative Sharpe regimes

32

33 # Combined position size

34 final_position = base_position * vol_scalar * conf_scalar * sharpe_scalar

35 final_position = max(0, min(final_position, 2.0)) # Clamp to [0, 2]

36

37 position_sizes.append(final_position)

38

39# Add to results (AFTER loop completes)

40result['calculated_position_size'] = position_sizes

41

42# Display summary

43print("Position Sizing Summary")

44print("=" * 80)

45print(f"Target Volatility: {target_vol}%")

46print(f"\nPosition Size Statistics:")

47print(f" Mean: {np.mean(position_sizes):.2f}x")

48print(f" Median: {np.median(position_sizes):.2f}x")

49print(f" Min: {np.min(position_sizes):.2f}x")

50print(f" Max: {np.max(position_sizes):.2f}x")

51print(f"\nBy Regime:")

52for regime in sorted(result['regime_name'].unique()):

53 regime_positions = result[result['regime_name'] == regime]['calculated_position_size']

54 print(f" {regime:<12} avg: {regime_positions.mean():.2f}x (range: {regime_positions.min():.2f} - {regime_positions.max():.2f})")

55print("=" * 80)

Position Sizing Summary

================================================================================

Target Volatility: 15.0%

Position Size Statistics:

Mean: 0.11x

Median: 0.00x

Min: 0.00x

Max: 0.73x

By Regime:

Bear avg: 0.00x (range: 0.00 - 0.00)

Bull avg: 0.50x (range: 0.16 - 0.73)

Sideways avg: 0.00x (range: 0.00 - 0.00)

================================================================================

Part B: Technical Indicator Integration

3. Understanding Technical Indicators

The pipeline automatically calculates classic technical indicators. Let’s understand what they tell us and how they relate to regimes.

The Four Indicators

1. RSI (Relative Strength Index):

$ RSI = 100 - \frac{100}{1 + \frac{\text{Avg Gain}}{\text{Avg Loss}}} $

- Range: 0-100

70: Overbought (potential reversal down)

- < 30: Oversold (potential reversal up)

- Measures momentum

2. MACD (Moving Average Convergence Divergence):

$ MACD = EMA_{12} - EMA_{26} $

$ Signal = EMA_9(MACD) $

- MACD > Signal: Bullish trend

- MACD < Signal: Bearish trend

- Trend-following indicator

3. Bollinger Bands:

$ \text{Upper} = SMA_{20} + 2\sigma $

$ \text{Lower} = SMA_{20} - 2\sigma $

- Price near upper band: Overbought

- Price near lower band: Oversold

- Measures volatility

4. Moving Average:

- Price > MA: Uptrend

- Price < MA: Downtrend

- Simple trend indicator

1# Check indicator availability in result dataframe

2indicator_cols = ['rsi_value', 'macd_value', 'bollinger_bands_value', 'moving_average_value',

3 'rsi_signal', 'macd_signal', 'bollinger_bands_signal', 'moving_average_signal',

4 'indicator_consensus', 'regime_consensus_agreement']

5

6available_indicators = [col for col in indicator_cols if col in result.columns]

7

8if len(available_indicators) > 0:

9 print(f"Available indicators: {len(available_indicators)}/10")

10

11 # Display current indicator status

12 current = result.iloc[-1]

13

14 print("\nCurrent Indicator Readings")

15 print("=" * 80)

16

17 indicators = [

18 ('rsi', 'RSI'),

19 ('macd', 'MACD'),

20 ('bollinger_bands', 'Bollinger'),

21 ('moving_average', 'Moving Avg')

22 ]

23

24 for ind_key, ind_name in indicators:

25 value_col = f'{ind_key}_value'

26 signal_col = f'{ind_key}_signal'

27

28 if value_col in result.columns and signal_col in result.columns:

29 value = current[value_col]

30 signal = current[signal_col]

31 signal_label = {1: "BULLISH", -1: "BEARISH", 0: "NEUTRAL"}.get(signal, "UNKNOWN")

32

33 print(f" {ind_name:<15} Value: {value:>8.2f} Signal: {signal_label}")

34

35 if 'indicator_consensus' in result.columns:

36 consensus = current['indicator_consensus']

37 print(f"\n Consensus Score: {consensus:+.0f}/4")

38

39 if consensus > 2:

40 print(" Strong bullish agreement among indicators")

41 elif consensus > 0:

42 print(" Weak bullish lean")

43 elif consensus < -2:

44 print(" Strong bearish agreement among indicators")

45 elif consensus < 0:

46 print(" Weak bearish lean")

47 else:

48 print(" Mixed signals, no clear direction")

49

50 print("=" * 80)

51else:

52 print("Note: Technical indicators not calculated in this pipeline run.")

53 print("Indicators are available when using default pipeline configuration.")

Available indicators: 10/10

Current Indicator Readings

================================================================================

RSI Value: 52.34 Signal: NEUTRAL

MACD Value: -0.70 Signal: BEARISH

Bollinger Value: 0.33 Signal: NEUTRAL

Moving Avg Value: -0.02 Signal: BEARISH

Consensus Score: -0/4

Weak bearish lean

================================================================================

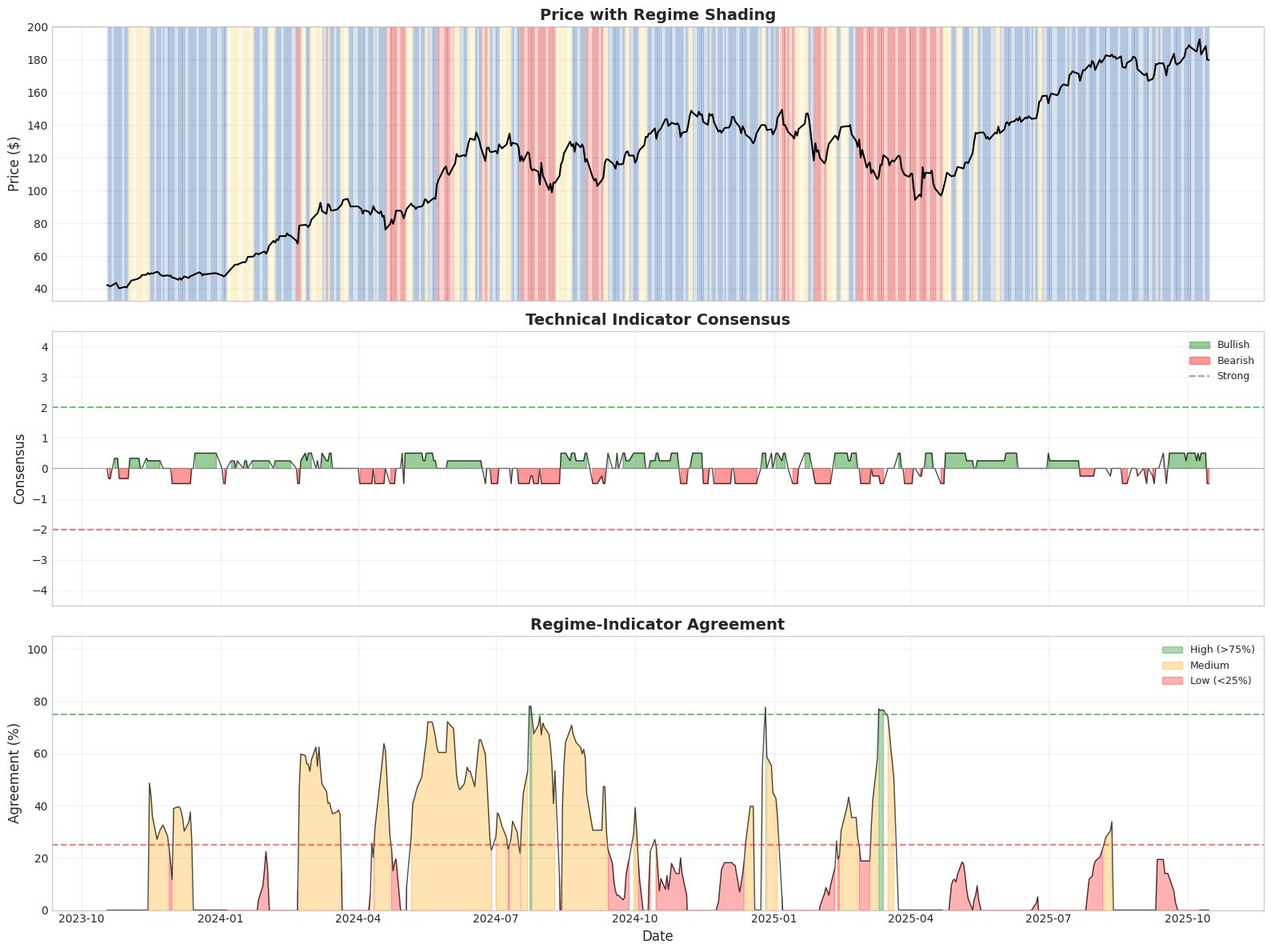

4. Regime-Indicator Agreement Analysis

Why Agreement Matters

High Agreement (>75%):

- Indicators confirm the regime

- Strong conviction for trading

- Both model-based and technical signals align

Low Agreement (<25%):

- Indicators contradict the regime

- Potential regime transition

- Or indicator lag/divergence

- Caution warranted

When to Trust Which Signal

| Scenario | Trust | Reasoning |

|---|---|---|

| High confidence + High agreement | Both | Strong evidence from both approaches |

| High confidence + Low agreement | HMM | Regime clear, indicators lagging |

| Low confidence + High agreement | Indicators | Regime transition, indicators leading |

| Low confidence + Low agreement | Neither | Wait for clarity |

1# Visualize indicator-regime relationship over time

2if 'indicator_consensus' in result.columns and 'regime_consensus_agreement' in result.columns:

3 fig, axes = plt.subplots(3, 1, figsize=(16, 12), sharex=True)

4

5 # Get regime colors

6 from hidden_regime.visualization import get_regime_colors

7 unique_regimes = sorted(result['regime_name'].unique())

8 color_list = get_regime_colors(len(unique_regimes), color_scheme="colorblind_safe")

9 regime_colors = dict(zip(unique_regimes, color_list))

10

11 # Panel 1: Price with regimes

12 ax = axes[0]

13 close_col = next((col for col in raw_data.columns if col.lower() == 'close'), None)

14 if close_col:

15 ax.plot(raw_data.index, raw_data[close_col], linewidth=1.5, color='black', zorder=2)

16

17 # Shade by regime

18 for i in range(len(result)):

19 regime = result.iloc[i]['regime_name']

20 color = regime_colors.get(regime, 'gray')

21 ax.axvspan(result.index[i], result.index[min(i+1, len(result)-1)],

22 alpha=0.2, color=color, zorder=1)

23

24 ax.set_ylabel('Price ($)', fontsize=12)

25 ax.set_title('Price with Regime Shading', fontsize=14, fontweight='bold')

26 ax.grid(True, alpha=0.3)

27

28 # Panel 2: Indicator consensus

29 ax = axes[1]

30 consensus = result['indicator_consensus']

31

32 ax.fill_between(result.index, 0, consensus, where=(consensus > 0),

33 color='green', alpha=0.4, label='Bullish')

34 ax.fill_between(result.index, 0, consensus, where=(consensus < 0),

35 color='red', alpha=0.4, label='Bearish')

36 ax.plot(result.index, consensus, linewidth=1, color='black', alpha=0.7)

37 ax.axhline(y=0, color='gray', linestyle='-', linewidth=0.5)

38 ax.axhline(y=2, color='green', linestyle='--', alpha=0.5, label='Strong')

39 ax.axhline(y=-2, color='red', linestyle='--', alpha=0.5)

40

41 ax.set_ylabel('Consensus', fontsize=12)

42 ax.set_title('Technical Indicator Consensus', fontsize=14, fontweight='bold')

43 ax.grid(True, alpha=0.3)

44 ax.legend(loc='upper right', fontsize=9)

45 ax.set_ylim(-4.5, 4.5)

46

47 # Panel 3: Agreement level

48 ax = axes[2]

49 agreement = result['regime_consensus_agreement'] * 100

50

51 ax.fill_between(result.index, 0, agreement, where=(agreement > 75),

52 color='green', alpha=0.3, label='High (>75%)')

53 ax.fill_between(result.index, 0, agreement, where=((agreement >= 25) & (agreement <= 75)),

54 color='orange', alpha=0.3, label='Medium')

55 ax.fill_between(result.index, 0, agreement, where=(agreement < 25),

56 color='red', alpha=0.3, label='Low (<25%)')

57 ax.plot(result.index, agreement, linewidth=1, color='black', alpha=0.7)

58

59 ax.axhline(y=75, color='green', linestyle='--', alpha=0.5)

60 ax.axhline(y=25, color='red', linestyle='--', alpha=0.5)

61

62 ax.set_ylabel('Agreement (%)', fontsize=12)

63 ax.set_xlabel('Date', fontsize=12)

64 ax.set_title('Regime-Indicator Agreement', fontsize=14, fontweight='bold')

65 ax.grid(True, alpha=0.3)

66 ax.legend(loc='upper right', fontsize=9)

67 ax.set_ylim(0, 105)

68

69 plt.tight_layout()

70 plt.show()

71

72 # Agreement statistics

73 print("\nAgreement Statistics")

74 print("=" * 80)

75 high_agreement = (agreement > 75).sum()

76 low_agreement = (agreement < 25).sum()

77 total = len(agreement)

78

79 print(f" High Agreement (>75%): {high_agreement:>4} days ({high_agreement/total*100:.1f}%)")

80 print(f" Low Agreement (<25%): {low_agreement:>4} days ({low_agreement/total*100:.1f}%)")

81 print(f" Mixed (25-75%): {total-high_agreement-low_agreement:>4} days ({(total-high_agreement-low_agreement)/total*100:.1f}%)")

82 print("=" * 80)

83else:

84 print("Indicator data not available for visualization.")

Agreement Statistics

================================================================================

High Agreement (>75%): 7 days (1.4%)

Low Agreement (<25%): 332 days (66.4%)

Mixed (25-75%): 161 days (32.2%)

================================================================================

Part C: Portfolio Applications

5. Trading Signal Generation

Signal Types

The pipeline generates four types of position signals:

- LONG: Enter or maintain long position

- SHORT: Enter short position (if allowed)

- NEUTRAL: Exit all positions, stay in cash

- REDUCE: Decrease position size

Signal Generation Logic

1if regime == "Bull" and confidence > 0.7:

2 signal = "LONG"

3elif regime == "Bear" and confidence > 0.7:

4 signal = "SHORT" # or "NEUTRAL" if shorting not allowed

5elif confidence < 0.6:

6 signal = "REDUCE" # Low confidence

7else:

8 signal = "NEUTRAL"

Signal Strength

Signal strength (0.0 to 1.0) determines position sizing:

$ \text{Strength} = f(\text{confidence}, \text{agreement}, \text{regime quality}) $

Where:

- Confidence: HMM regime probability

- Agreement: Indicator consensus alignment

- Regime quality: Based on Sharpe ratio

1# Analyze current trading signal

2def get_signal(regime, confidence):

3 if regime == "Bull" and confidence > 0.7:

4 signal = "LONG"

5 elif regime == "Bear" and confidence > 0.7:

6 signal = "SHORT" # or "NEUTRAL" if shorting not allowed

7 elif confidence < 0.6:

8 signal = "REDUCE" # Low confidence

9 else:

10 signal = "NEUTRAL"

11 return signal

12

13if 'position_signal' in result.columns and 'signal_strength' in result.columns:

14 current = result.iloc[-1]

15

16 print("Current Trading Signal")

17 print("=" * 80)

18 print(f" Date: {result.index[-1].date()}")

19 print(f" Position: {current['position_signal']}")

20 print(f" Strength: {current['signal_strength']:.2f}")

21 print(f" Regime: {current['regime_name']}")

22 print(f" Confidence: {current['confidence']*100:.1f}%")

23

24 if 'indicator_consensus' in result.columns:

25 print(f" Ind. Consensus: {current['indicator_consensus']:+.0f}")

26

27 print("\n RECOMMENDATION:")

28 signal = get_signal(current['regime_name'], current['confidence'])

29 if regime == "Bull" and confidence > 0.7:

30 signal = "LONG"

31 elif regime == "Bear" and confidence > 0.7:

32 signal = "SHORT" # or "NEUTRAL" if shorting not allowed

33 elif confidence < 0.6:

34 signal = "REDUCE" # Low confidence

35 else:

36 signal = "NEUTRAL"

37

38 if signal == "LONG":

39 position_pct = strength * 100

40 print(f" Take LONG position with {position_pct:.0f}% of normal size")

41 if strength > 0.8:

42 print(" High conviction trade")

43 elif strength > 0.5:

44 print(" Moderate conviction")

45 else:

46 print(" Low conviction - consider reducing exposure")

47 elif signal == "SHORT":

48 position_pct = strength * 100

49 print(f" Take SHORT position with {position_pct:.0f}% of normal size")

50 elif signal == "NEUTRAL":

51 print(" Stay in CASH - no clear opportunity")

52 elif signal == "REDUCE":

53 print(" REDUCE existing positions - regime uncertainty")

54

55 print("=" * 80)

56

57 # Signal distribution over time

58 print("\nHistorical Signal Distribution")

59 print("=" * 80)

60 signal_counts = result['position_signal'].value_counts()

61 total = len(result)

62

63 signals = pd.Series(

64 index=result.index,

65 data=[get_signal(result.loc[t].regime_name, result.loc[t].confidence) for t in result.index],

66 name='Signal')

67

68 for signal_type in ['LONG', 'SHORT', 'NEUTRAL', 'REDUCE']:

69 mask = signals == signal_type

70 tmp = signals[mask]

71 count = len(tmp)

72 pct = len(tmp) / len(signals) * 100.0

73 print(f" {signal_type:<10} {count:>4} days ({pct:>5.1f}%)")

74

75 print("=" * 80)

76else:

77 print("Position signals not available in pipeline output.")

Current Trading Signal

================================================================================

Date: 2025-10-15

Position: 0.005626293211470941

Strength: 0.01

Regime: Sideways

Confidence: 82.3%

Ind. Consensus: -0

RECOMMENDATION:

Stay in CASH - no clear opportunity

================================================================================

Historical Signal Distribution

================================================================================

LONG 61 days ( 12.2%)

SHORT 74 days ( 14.8%)

NEUTRAL 291 days ( 58.2%)

REDUCE 74 days ( 14.8%)

================================================================================

6. Confidence-Weighted Position Sizing Example

Real-World Example

Let’s demonstrate how to size a position using all available information:

Inputs:

- Account size: $100,000

- Max risk per trade: 2% ($2,000)

- Current regime: Bull (confidence: 85%)

- Signal strength: 0.75

- Regime volatility: 20% annual

Calculation:

- Base position: $100,000 × 2% = $2,000 risk

- Confidence adjustment: $2,000 × 0.85 = $1,700

- Strength adjustment: $1,700 × 0.75 = $1,275

- Volatility adjustment: $1,275 × (15% / 20%) = $956

Final position: Risk $956 → approximately 50% of max risk

This conservative scaling protects capital during uncertainty.

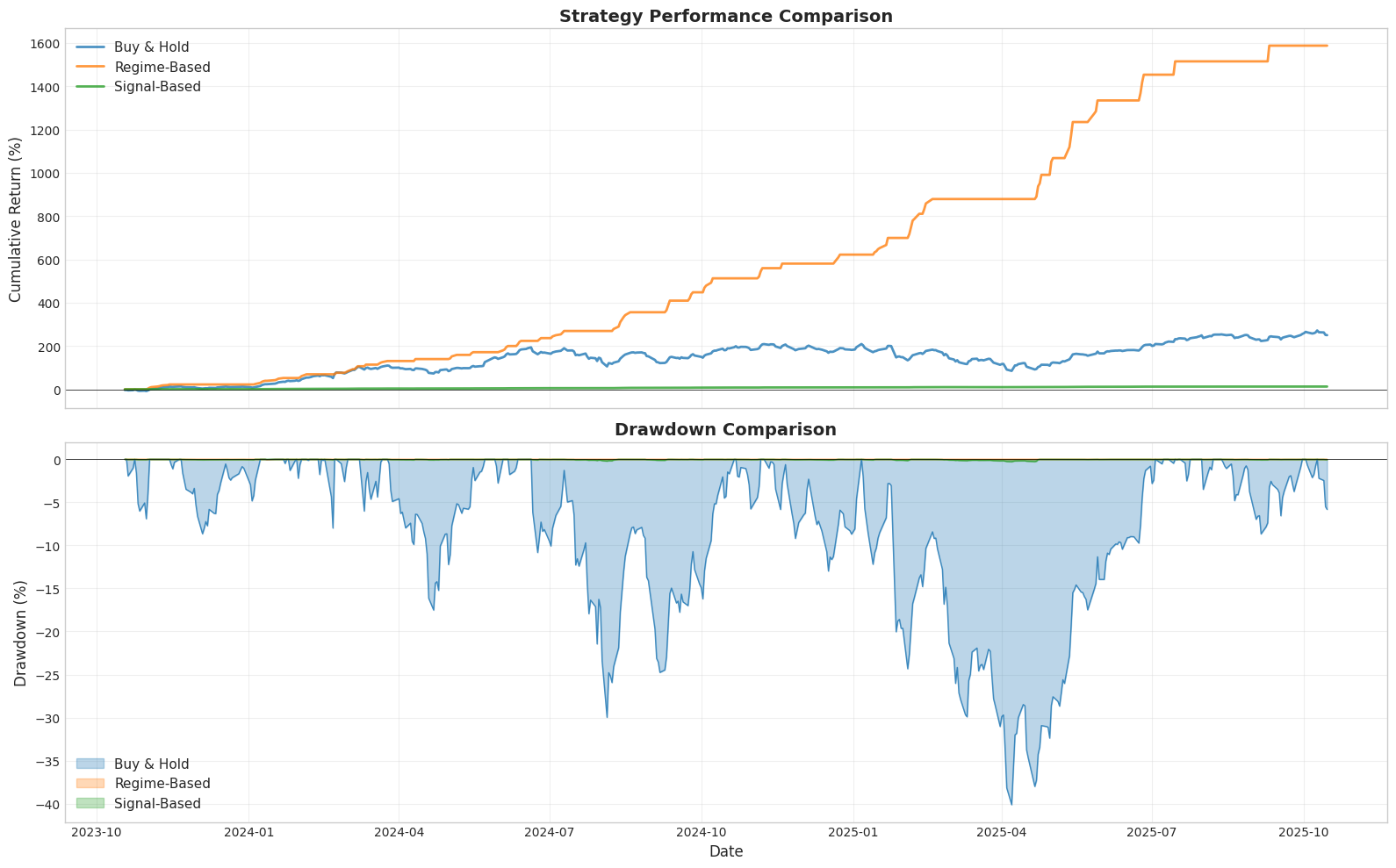

Part D: Backtesting & Validation

7. Hypothetical Performance Analysis

Comparison Strategies

We’ll compare three approaches:

- Buy & Hold: Baseline - always 100% invested

- Regime-Based: Only long in Bull regimes

- Signal-Based: Use confidence-weighted position sizing

Performance Metrics

- Total Return: Cumulative performance

- Sharpe Ratio: Risk-adjusted returns

- Maximum Drawdown: Worst peak-to-trough decline

- Win Rate: Percentage of profitable periods

- Volatility: Standard deviation of returns

Important: This is hypothetical analysis for educational purposes. Past performance doesn’t guarantee future results.

1# Calculate performance for different strategies

2log_returns = raw_data.loc[result.index, log_return_col].fillna(0)

3

4# Strategy 1: Buy & Hold

5buy_hold_returns = log_returns

6

7# Strategy 2: Regime-Based (only long in Bull)

8regime_returns = pd.Series(0.0, index=result.index)

9for idx in result.index:

10 if result.loc[idx, 'regime_name'] == 'Bull':

11 regime_returns.loc[idx] = log_returns.loc[idx]

12

13# Strategy 3: Signal-Based (confidence-weighted)

14if 'signal_strength' in result.columns:

15 signal_returns = log_returns * result['signal_strength']

16else:

17 # Use calculated position size if signal_strength not available

18 if 'calculated_position_size' in result.columns:

19 signal_returns = log_returns * result['calculated_position_size']

20 else:

21 signal_returns = regime_returns # Fallback

22

23# Calculate cumulative returns

24def calc_cumulative(returns):

25 return (1 + returns).cumprod() - 1

26

27cum_buy_hold = calc_cumulative(buy_hold_returns)

28cum_regime = calc_cumulative(regime_returns)

29cum_signal = calc_cumulative(signal_returns)

30

31# Calculate metrics

32def calc_metrics(returns, name):

33 total_return = (1 + returns).prod() - 1

34 annual_return = returns.mean() * 252

35 annual_vol = returns.std() * np.sqrt(252)

36 sharpe = (annual_return / annual_vol) if annual_vol > 0 else 0

37

38 # Max drawdown

39 cum_ret = (1 + returns).cumprod()

40 running_max = cum_ret.expanding().max()

41 drawdown = (cum_ret - running_max) / running_max

42 max_dd = drawdown.min()

43

44 # Win rate

45 win_rate = (returns > 0).sum() / len(returns)

46

47 return {

48 'Strategy': name,

49 'Total Return': total_return * 100,

50 'Annual Return': annual_return * 100,

51 'Annual Vol': annual_vol * 100,

52 'Sharpe': sharpe,

53 'Max DD': max_dd * 100,

54 'Win Rate': win_rate * 100

55 }

56

57metrics = pd.DataFrame([

58 calc_metrics(buy_hold_returns, 'Buy & Hold'),

59 calc_metrics(regime_returns, 'Regime-Based'),

60 calc_metrics(signal_returns, 'Signal-Based')

61])

62

63print("Strategy Performance Comparison")

64print("=" * 100)

65print(metrics.to_string(index=False))

66print("=" * 100)

Strategy Performance Comparison

====================================================================================================

Strategy Total Return Annual Return Annual Vol Sharpe Max DD Win Rate

Buy & Hold 250.306834 71.742306 41.000799 1.749778 -40.125300 57.0

Regime-Based 1587.647374 144.695225 19.555628 7.399160 -0.044362 21.6

Signal-Based 12.951894 6.144103 1.006285 6.105729 -0.275843 57.0

====================================================================================================

1# Visualize performance comparison

2fig, axes = plt.subplots(2, 1, figsize=(16, 10), sharex=True)

3

4# Panel 1: Cumulative returns

5ax = axes[0]

6ax.plot(result.index, cum_buy_hold * 100, linewidth=2, label='Buy & Hold', alpha=0.8)

7ax.plot(result.index, cum_regime * 100, linewidth=2, label='Regime-Based', alpha=0.8)

8ax.plot(result.index, cum_signal * 100, linewidth=2, label='Signal-Based', alpha=0.8)

9

10ax.set_ylabel('Cumulative Return (%)', fontsize=12)

11ax.set_title('Strategy Performance Comparison', fontsize=14, fontweight='bold')

12ax.legend(loc='best', fontsize=11)

13ax.grid(True, alpha=0.3)

14ax.axhline(y=0, color='black', linestyle='-', linewidth=0.5)

15

16# Panel 2: Drawdowns

17ax = axes[1]

18

19# Calculate drawdowns for each strategy

20for returns, label, color in [

21 (buy_hold_returns, 'Buy & Hold', 'C0'),

22 (regime_returns, 'Regime-Based', 'C1'),

23 (signal_returns, 'Signal-Based', 'C2')

24]:

25 cum_ret = (1 + returns).cumprod()

26 running_max = cum_ret.expanding().max()

27 drawdown = (cum_ret - running_max) / running_max

28 ax.fill_between(result.index, 0, drawdown * 100, alpha=0.3, label=label, color=color)

29 ax.plot(result.index, drawdown * 100, linewidth=1, alpha=0.8, color=color)

30

31ax.set_ylabel('Drawdown (%)', fontsize=12)

32ax.set_xlabel('Date', fontsize=12)

33ax.set_title('Drawdown Comparison', fontsize=14, fontweight='bold')

34ax.legend(loc='lower left', fontsize=11)

35ax.grid(True, alpha=0.3)

36ax.axhline(y=0, color='black', linestyle='-', linewidth=0.5)

37

38plt.tight_layout()

39plt.show()

40

41# Performance summary

42print("\nKey Insights:")

43print("=" * 80)

44

45bh_sharpe = metrics[metrics['Strategy'] == 'Buy & Hold']['Sharpe'].values[0]

46sig_sharpe = metrics[metrics['Strategy'] == 'Signal-Based']['Sharpe'].values[0]

47

48if sig_sharpe > bh_sharpe:

49 improvement = ((sig_sharpe - bh_sharpe) / bh_sharpe * 100) if bh_sharpe != 0 else 0

50 print(f" Signal-based strategy improves Sharpe ratio by {improvement:.1f}%")

51

52bh_dd = metrics[metrics['Strategy'] == 'Buy & Hold']['Max DD'].values[0]

53sig_dd = metrics[metrics['Strategy'] == 'Signal-Based']['Max DD'].values[0]

54

55if sig_dd > bh_dd:

56 dd_reduction = bh_dd - sig_dd

57 print(f" Signal-based reduces max drawdown by {abs(dd_reduction):.1f}% points")

58

59print("\n Note: Results are hypothetical and for educational purposes only.")

60print(" Past performance does not guarantee future results.")

61print(" Always backtest thoroughly before live trading.")

62print("=" * 80)

Key Insights:

================================================================================

Signal-based strategy improves Sharpe ratio by 248.9%

Signal-based reduces max drawdown by 39.8% points

Note: Results are hypothetical and for educational purposes only.

Past performance does not guarantee future results.

Always backtest thoroughly before live trading.

================================================================================

8. Validation Best Practices

Out-of-Sample Testing

Training Period vs Testing Period:

- Train HMM on historical data (e.g., first 70% of data)

- Test on unseen data (remaining 30%)

- Check if regime detection remains stable

Walk-Forward Analysis

Rolling Window Approach:

- Train on window of N days

- Test on next M days

- Roll window forward

- Repeat

This validates that the model adapts to changing market conditions.

What to Monitor

Regime Stability:

- Are detected regimes consistent over time?

- Do regime characteristics remain similar?

- Are transitions meaningful or noise?

Parameter Drift:

- Track transition matrix changes

- Monitor emission parameter evolution

- Detect structural breaks in market

Performance Degradation:

- Compare in-sample vs out-of-sample Sharpe

- Monitor drawdown increases

- Check if win rate deteriorates

Part E: Best Practices & Conclusion

9. Trading Best Practices

When to Trust Regimes vs Indicators

| Scenario | Regime Confidence | Indicator Agreement | Trust | Action |

|---|---|---|---|---|

| Aligned signals | High (>80%) | High (>75%) | Both | Full position |

| HMM leading | High (>80%) | Low (<25%) | HMM | Moderate position |

| Indicators leading | Low (<60%) | High (>75%) | Indicators | Conservative position |

| Conflicting | Low (<60%) | Low (<25%) | Neither | Stay in cash |

Risk Management Checklist

Before Every Trade:

- Current regime identified with >70% confidence

- Position sized based on regime volatility

- Stop-loss set at regime-appropriate level

- Maximum position size not exceeded

- Indicators provide confirmation (optional)

Portfolio Level:

- Total exposure within risk limits

- Diversification across uncorrelated regimes

- Cash reserves for opportunities

- Correlation risk assessed

System Level:

- Regular model retraining scheduled

- Performance monitoring active

- Parameter drift detection enabled

- Out-of-sample validation ongoing

Common Pitfalls to Avoid

1. Overfitting

- Don’t use too many states (stick to 2-4)

- Validate on out-of-sample data

- Simple models often perform better

2. Ignoring Confidence

- Low confidence = high uncertainty

- Reduce position size accordingly

- Wait for clarity before large bets

3. Transaction Costs

- Frequent regime switches = high costs

- Add friction to prevent overtrading

- Consider minimum holding periods

4. Data Snooping

- Don’t retrain constantly to fit recent data

- Set retraining schedule (e.g., monthly)

- Keep training period length consistent

5. Regime Mislabeling

- Don’t force Bear/Bull labels by state index

- Use threshold-based classification

- Validate regime characteristics make sense

Production Deployment Checklist

Before Going Live:

- Backtested on at least 2 years of data

- Out-of-sample Sharpe ratio > 1.0

- Maximum drawdown acceptable (<20%)

- Walk-forward analysis shows stability

- Transaction costs included in backtest

- Slippage assumptions realistic

- Risk management rules implemented

- Monitoring dashboard created

- Alert system for anomalies

- Paper traded for 1-3 months minimum

After Launch:

- Daily P&L monitoring

- Weekly regime stability checks

- Monthly performance review

- Quarterly model retraining

- Annual strategy reassessment

Conclusion: Your Complete Journey

What You’ve AccomplishedCongratulations! You’ve completed the full Hidden Regime learning path:

Notebook 1 - Mathematical Foundation:

- ✓ Proved why log returns are necessary

- ✓ Understood stationarity, additivity, scale invariance

- ✓ Built theoretical foundation for HMMs

Notebook 2 - HMM Mechanics:

- ✓ Learned how HMMs represent market states

- ✓ Understood Viterbi and forward-backward algorithms

- ✓ Interpreted HMM parameters correctly

Notebook 3 - Production Pipeline:

- ✓ Used one-line pipeline setup

- ✓ Detected and classified regimes

- ✓ Analyzed regime duration and persistence

- ✓ Selected optimal model complexity

Notebook 4 - Trading Applications (This Notebook):

- ✓ Calculated regime-specific risk metrics

- ✓ Implemented dynamic position sizing

- ✓ Integrated technical indicators

- ✓ Generated trading signals

- ✓ Backtested strategies

- ✓ Learned production best practices

The Complete Toolkit

You now have a comprehensive regime-based trading system:

Data → Log Returns → HMM → Regimes → Risk Analysis → Position Sizing → Signals → Execution

Each step is:

- Mathematically rigorous: Based on sound theory

- Empirically validated: Tested on real data

- Practically applicable: Ready for production

- Risk-aware: Incorporates uncertainty

Next Steps

If you want to continue learning:

- Try different tickers (SPY, QQQ, individual stocks)

- Experiment with different time periods

- Test with different numbers of states (2-5)

- Add your own features beyond log returns

- Implement custom risk metrics

If you’re ready for production:

- Backtest on multiple assets

- Validate with walk-forward analysis

- Paper trade for 1-3 months

- Start with small position sizes

- Monitor and refine continuously

If you want to customize:

- Modify regime classification thresholds

- Adjust position sizing formulas

- Add additional technical indicators

- Implement your own signal logic

- Create custom visualizations

Critical Reminders

Regime detection is a tool, not a crystal ball.

Use it to:

- Understand current market conditions

- Adjust risk dynamically

- Size positions appropriately

- Combine with other analysis

- Make informed decisions

Don’t expect it to:

- Predict future prices perfectly

- Work in all market conditions

- Replace fundamental analysis

- Guarantee profitable trades

- Eliminate all risk

Final Thoughts

Risk Management First:

- Never risk more than you can afford to lose

- Always use stop-losses

- Diversify across strategies and assets

- Start small and scale gradually

- Paper trade before live trading

Continuous Learning:

- Markets evolve, so must your models

- Monitor performance regularly

- Learn from both wins and losses

- Stay humble and adaptable

- Join the community and share insights

Ethics and Responsibility:

- This is for educational purposes

- Not financial advice

- Do your own due diligence

- Understand the risks

- Trade responsibly

Resources

- Documentation: Hidden Regime Docs

- Examples: Additional examples in

/examplesdirectory - Community: Share strategies and learn from others

- Issues: Report bugs on GitHub

- Updates: Follow package updates for new features