HMM Basics

HMM Basics: Understanding Regime Detection

From Log Returns to Market Regimes Using Hidden Markov Models

In the previous notebook, we proved that log returns are the correct transformation for financial time series.

Now we’ll use those log returns to detect market regimes using **Hidden Markov Models (HMMs)** .

What You’ll Learn

- What HMMs are and how they work

- What parameters HMMs learn from data

- How to interpret HMM states (WITHOUT forcing Bull/Bear labels)

- How to choose the right number of states

- How to visualize regime sequences

Important Note

This notebook uses minimal code to understand HMM mechanics. GitHub

Next notebook shows the full library pipeline with analysis tools and best practices.

1import sys

2from pathlib import Path

3import numpy as np

4import pandas as pd

5import matplotlib.pyplot as plt

6import seaborn as sns

7from datetime import datetime, timedelta

8import warnings

9warnings.filterwarnings('ignore')

10

11# Add parent to path

12sys.path.insert(0, str(Path().absolute().parent))

13

14# Hidden Regime imports - minimal

15from hidden_regime.data import FinancialDataLoader

16from hidden_regime.observations import FinancialObservationGenerator

17from hidden_regime.models import HiddenMarkovModel

18from hidden_regime.config import FinancialDataConfig, FinancialObservationConfig, HMMConfig

19from hidden_regime.utils import log_return_to_percent_change

20

21# Plotting

22plt.style.use('seaborn-v0_8-whitegrid')

23sns.set_palette("husl")

1. What is a Hidden Markov Model?

The Core Idea

An HMM assumes the market operates in hidden states (regimes) that we cannot directly observe. Each regime has:

- Different return characteristics (mean and volatility)

- Persistence (tendency to stay in the same regime)

- Transition probabilities (likelihood of switching to other regimes)

The Three Components

- Hidden States $(S_1, S_2, ..., S_t)$: The unobserved regime sequence

- Observations $(O_1, O_2, ..., O_t)$: The log returns we can see

- Parameters:

- **Transition Matrix** $A_{ij}: P(regime(t+1) = j\ |\ regime(t) = i)$. Note that this is a stochastic matrix in that each row sums to exactly $1$ (this is because, from any given state, the probability of transitioning to all possible states must sum to $1$. $\sum_{j} A_{ij} = 1$)

- Emission Means $\mu$: Average log return for each Regime

- Emission Stds $\sigma$: Volatility for each regime

- **Initial Probs** $\pi$: Starting regime distribution

What HMMs Do

Given observed log returns, HMMs simultaneously:

- Infer the most likely regime sequence (states)

- Learn the transition probabilities (how regimes switch)

- Learn emission parameters (return characteristics of each regime)

2. Load Data and Create Observations

We’ll use NVDA (NVIDIA) with 2 years of data. NVDA is more volatile than SPY, showing clearer regime transitions.

1# Configure data loader

2data_config = FinancialDataConfig(

3 ticker='NVDA',

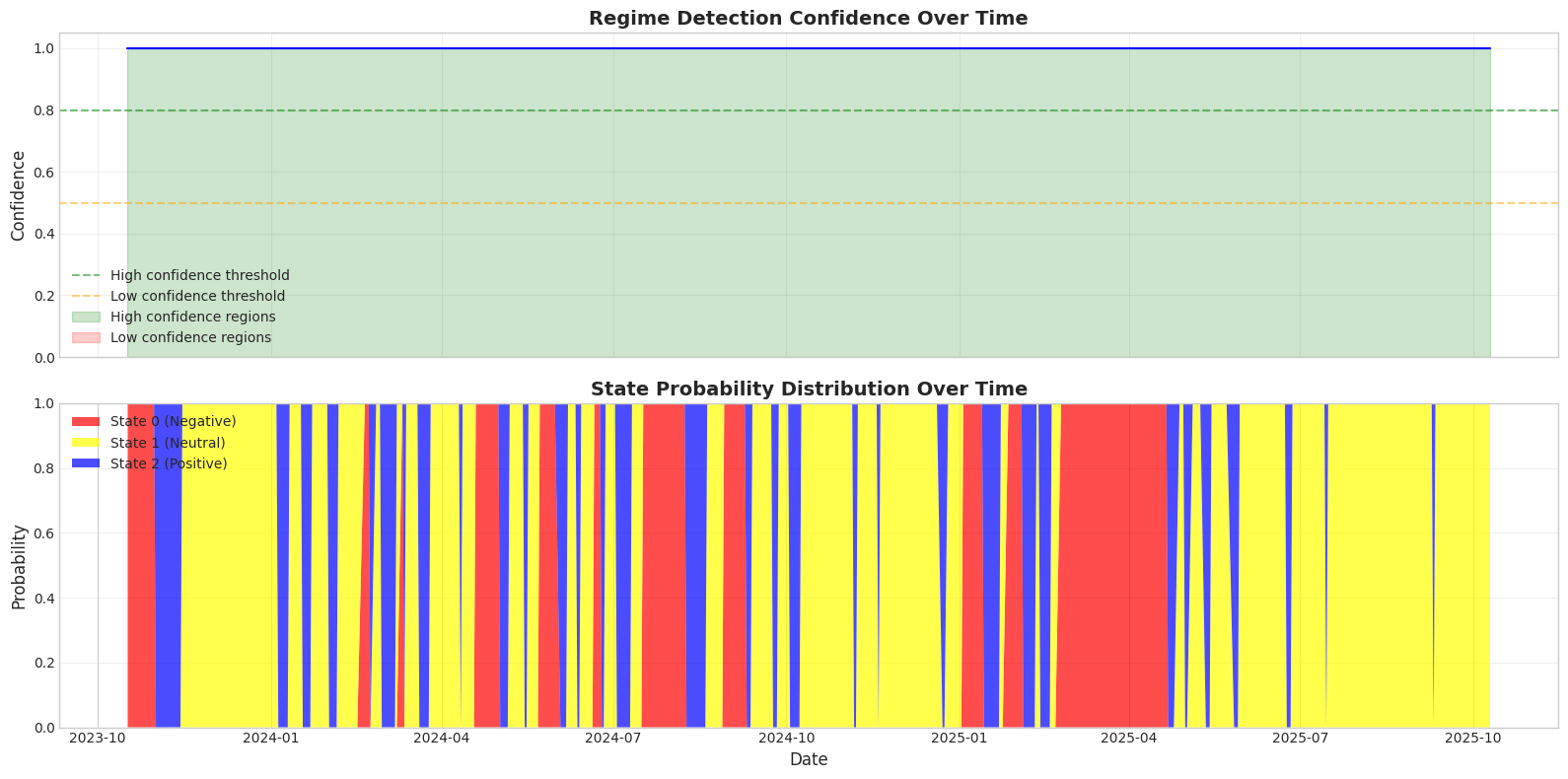

4 end_date=datetime.now(),

5 num_samples=504 # ~2 years of trading days

6)

7

8# Load data

9loader = FinancialDataLoader(data_config)

10df = loader.load_data()

11

12print(f"Loaded {len(df)} days of NVDA data")

13print(f"Date range: {df.index[0].date()} to {df.index[-1].date()}")

14print(f"\nData columns: {list(df.columns)}")

15print(f"\nFirst few rows:")

16print(df.head())

Loaded 498 days of NVDA data

Date range: 2023-10-17 to 2025-10-10

Data columns: ['open', 'high', 'low', 'close', 'volume', 'price', 'pct_change', 'log_return']

First few rows:

open high low close \

Date

2023-10-17 00:00:00-04:00 43.974085 44.727642 42.454979 43.912121

2023-10-18 00:00:00-04:00 42.565910 43.193543 41.800363 42.171143

2023-10-19 00:00:00-04:00 42.785783 43.271497 41.857330 42.076202

2023-10-20 00:00:00-04:00 41.865319 42.444980 41.053798 41.362617

2023-10-23 00:00:00-04:00 41.204718 43.222530 40.920885 42.949688

volume price pct_change log_return

Date

2023-10-17 00:00:00-04:00 812333000 43.767207 -0.039074 -0.039858

2023-10-18 00:00:00-04:00 627294000 42.432740 -0.030490 -0.030965

2023-10-19 00:00:00-04:00 501233000 42.497703 0.001531 0.001530

2023-10-20 00:00:00-04:00 477266000 41.681679 -0.019202 -0.019388

2023-10-23 00:00:00-04:00 478530000 42.074455 0.009423 0.009379

3. Understanding State Probabilities (Preview)

HMMs Provide Two Types of Output

Before we train the model, it’s important to understand what HMMs give us:

1. Most Likely Path (Viterbi Algorithm )

- Single “best guess” state sequence:

[0, 0, 1, 2, 2, 1, ...] - Answers: “What regime was the market most likely in?”

- Fast to compute, easy to visualize

2. State Probability Distribution (Forward-Backward Algorithm )

- Full probability distribution for each day:

[0.85, 0.12, 0.03] - Answers: “How confident are we in each regime?”

- Critical for risk management and decision-making

Why Uncertainty Matters

Consider two scenarios with the same Viterbi path:

High Confidence: [0.95, 0.04, 0.01] → “Definitely in State 0”

- Clear regime signal

- Safe to make strong portfolio decisions

Low Confidence: [0.40, 0.35, 0.25] → “Probably State 0, but unclear”

- Regime transition likely happening

- Should reduce position sizes

What We’ll Show

After training the HMM, we’ll demonstrate:

- Viterbi path: For visualization and interpretation

- State probabilities: For confidence and risk assessment

Key Insight: The probability distribution is often more valuable than the single “best” state.

1# Create observation generator

2obs_config = FinancialObservationConfig(

3 generators=["log_return"], # Just log returns

4 price_column="close",

5 normalize_features=False # Keep raw log returns

6)

7

8obs_generator = FinancialObservationGenerator(obs_config)

9observations_df = obs_generator.update(df)

10

11# For HMM training, we need just the log_return column as a DataFrame

12observations = observations_df[['log_return']]

13

14print(f"Generated {len(observations)} observations")

15print(f"Observation shape: {observations.shape}")

16print(f"\nObservations are log returns:")

17print(f" Mean: {observations.values.mean():.6f}")

18print(f" Std: {observations.values.std():.6f}")

19print(f" Min: {observations.values.min():.6f}")

20print(f" Max: {observations.values.max():.6f}")

21

22# Convert a few examples to percentage for interpretation

23print(f"\nExample log returns converted to percentages:")

24for i in range(min(5, len(observations))):

25 log_ret = observations.iloc[i, 0]

26 pct = log_return_to_percent_change(log_ret) * 100

27 print(f" Day {i+1}: log_return={log_ret:.6f} → {pct:+.2f}%")

Generated 498 observations

Observation shape: (498, 1)

Observations are log returns:

Mean: 0.002853

Std: 0.025877

Min: -0.175225

Max: 0.124061

Example log returns converted to percentages:

Day 1: log_return=-0.039858 → -3.91%

Day 2: log_return=-0.030965 → -3.05%

Day 3: log_return=0.001530 → +0.15%

Day 4: log_return=-0.019388 → -1.92%

Day 5: log_return=0.009379 → +0.94%

4. Train the HMM

Now we’ll train a 3-state HMM on these log returns. The model will learn:

- Which regime the market was in each day

- The transition probabilities between regimes

- The mean return and volatility for each regime

1# Configure HMM with 3 states

2hmm_config = HMMConfig(

3 n_states=3,

4 max_iterations=100, # Maximum training iterations

5 tolerance=1e-4, # Convergence tolerance

6 random_seed=42

7)

8

9# Create and train model

10print("Training 3-state HMM...")

11hmm = HiddenMarkovModel(hmm_config)

12hmm.fit(observations)

13

14print(f"Training complete!")

15print(f" Converged: {hmm.training_history_['converged']}")

16print(f" Iterations: {hmm.training_history_['iterations']}")

17print(f" Final log-likelihood: {hmm.score(observations):.2f}")

Training 3-state HMM...

Training on 498 observations (removed 0 NaN values)

Training complete!

Converged: False

Iterations: 100

Final log-likelihood: -747.20

6. Interpreting the Parameters

What Do These Numbers Actually Mean?

Let’s translate the raw parameters into practical insights.

Transition Matrix Interpretation (Focus on diagonal):

From State 0 to State 0: 0.XXX → "Persistence probability"

The diagonal elements tell us how long regimes last:

- If $P(0|0) = 0.95$, then $Expected\ duration = \frac{1}{1-0.95} = 20\ days$

- If $P(0|0) = 0.80$, then $Expected\ duration = \frac{1}{1-0.80} = 5\ days$

Formula: $Expected\ duration = \frac{1}{1 - diagonal\ probability}$

Emission Parameters Interpretation:

For each state, we can calculate:

Daily Return (in %): Convert log space to percentage

- $mean\ pct = e^{mean\ log - 1} * 100$

Annualized Return (assuming 252 trading days):

- $annual\ return = (e^{mean\ log * 252} - 1) * 100$

Daily Volatility (in %):

- $vol\ pct = std\ log * 100$ (approximation valid for small returns)

Annualized Volatility:

- $annual\ vol = std\ log * \sqrt{252} * 100$ (assumes 252 trading days per year)

Example Interpretation

State 0 (using example numbers):

- Daily: -0.15% return, 2.5% volatility

- Annualized: -37% return, 40% volatility

- Duration: ~15 days

- Interpretation: “High volatility bear market that lasts 2-3 weeks”

State 1:

- Daily: +0.02% return, 1.2% volatility

- Annualized: +5% return, 19% volatility

- Duration: ~25 days

- Interpretation: “Low volatility sideways market, very persistent”

State 2:

- Daily: +0.18% return, 1.8% volatility

- Annualized: +54% return, 29% volatility

- Duration: ~8 days

- Interpretation: “Strong bull runs, but don’t last long”

Key Insight

The model discovered these patterns from data alone - we didn’t tell it what “bear” or “bull” means. The parameters quantify real market behavior.

5. Inspect Learned Parameters

Let’s see what the HMM learned about the three regimes.

1# First, we need to extract parameters and predict states

2# Extract learned parameters

3transition_matrix = hmm.transition_matrix_

4emission_means = hmm.emission_means_

5emission_stds = hmm.emission_stds_

6start_probs = hmm.initial_probs_

7

8print('Emission means: ', emission_means)

9print('Emission stds : ', emission_stds)

10

11# Sort by mean for easier interpretation

12sorted_idx = np.argsort(emission_means)

13

14# Predict states using Viterbi algorithm

15predictions_df = hmm.predict(observations)

16states = predictions_df['predicted_state'].values

17

18# Define colors and names for visualization

19state_colors = {sorted_idx[0]: 'red', sorted_idx[1]: 'yellow', sorted_idx[2]: 'blue'}

20state_names = {sorted_idx[0]: 'Negative', sorted_idx[1]: 'Neutral', sorted_idx[2]: 'Positive'}

21

22# Get dates

23dates = df.index

24log_returns = observations.values.flatten()

25

26# Now get state probabilities using forward-backward algorithm

27# This gives us P(state | all observations) for each time point

28state_probs = hmm.predict_proba(observations)

29

30print(f"State probability matrix shape: {state_probs.shape}")

31print(f" {state_probs.shape[0]} time points")

32print(f" {state_probs.shape[1]} states")

33print(f"\nEach row sums to 1.0 (probability distribution):")

34print(f" Row 0 sum: {state_probs.iloc[0].sum():.4f}")

35print(f" Row 100 sum: {state_probs.iloc[100].sum():.4f}")

36

37# Calculate confidence (max probability for each day)

38confidence = state_probs.max(axis=1).values

39

40print(f"\nConfidence Statistics:")

41print(f" Mean confidence: {confidence.mean():.2%}")

42print(f" Min confidence: {confidence.min():.2%}")

43print(f" Max confidence: {confidence.max():.2%}")

44

45# Find high and low confidence periods

46high_conf_idx = np.argmax(confidence)

47low_conf_idx = np.argmin(confidence)

48

49print(f"\nHighest Confidence Day:")

50print(f" Date: {dates[high_conf_idx+1].date()}")

51print(f" State: {states[high_conf_idx]}")

52print(f" Probabilities: {state_probs.iloc[high_conf_idx].values}")

53print(f" Confidence: {confidence[high_conf_idx]:.2%}")

54

55print(f"\nLowest Confidence Day (likely regime transition):")

56print(f" Date: {dates[low_conf_idx+1].date()}")

57print(f" State: {states[low_conf_idx]}")

58print(f" Probabilities: {state_probs.iloc[low_conf_idx].values}")

59print(f" Confidence: {confidence[low_conf_idx]:.2%}")

60

61# Visualize confidence over time

62fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(16, 8), sharex=True)

63

64# Top panel: Confidence over time

65ax1.plot(dates, confidence, linewidth=1.5, color='blue')

66ax1.axhline(y=0.8, color='green', linestyle='--', alpha=0.5, label='High confidence threshold')

67ax1.axhline(y=0.5, color='orange', linestyle='--', alpha=0.5, label='Low confidence threshold')

68ax1.fill_between(dates, 0, confidence, where=(confidence > 0.8), alpha=0.2, color='green', label='High confidence regions')

69ax1.fill_between(dates, 0, confidence, where=(confidence < 0.5), alpha=0.2, color='red', label='Low confidence regions')

70ax1.set_ylabel('Confidence', fontsize=12)

71ax1.set_title('Regime Detection Confidence Over Time', fontsize=14, fontweight='bold')

72ax1.legend(loc='lower left')

73ax1.grid(True, alpha=0.3)

74ax1.set_ylim(0, 1.05)

75

76# Bottom panel: State probabilities stacked

77ax2.stackplot(dates,

78 state_probs.iloc[:, sorted_idx[0]].values,

79 state_probs.iloc[:, sorted_idx[1]].values,

80 state_probs.iloc[:, sorted_idx[2]].values,

81 labels=[f'State {sorted_idx[0]} ({state_names[sorted_idx[0]]})',

82 f'State {sorted_idx[1]} ({state_names[sorted_idx[1]]})',

83 f'State {sorted_idx[2]} ({state_names[sorted_idx[2]]})'],

84 colors=[state_colors[sorted_idx[0]], state_colors[sorted_idx[1]], state_colors[sorted_idx[2]]],

85 alpha=0.7)

86ax2.set_ylabel('Probability', fontsize=12)

87ax2.set_xlabel('Date', fontsize=12)

88ax2.set_title('State Probability Distribution Over Time', fontsize=14, fontweight='bold')

89ax2.legend(loc='upper left')

90ax2.grid(True, alpha=0.3, axis='y')

91ax2.set_ylim(0, 1)

92

93plt.tight_layout()

94plt.show()

95

96print("\nKey Observations:")

97print("1. High confidence periods → clear regime signal")

98print("2. Low confidence periods → regime transitions happening")

99print("3. Stacked probabilities show regime evolution")

100print("4. For trading: reduce positions during low confidence periods")

Emission means: [-0.00889602 -0.00121936 0.02271938]

Emission stds : [0.04053647 0.0140285 0.01465051]

State probability matrix shape: (498, 3)

498 time points

3 states

Each row sums to 1.0 (probability distribution):

Row 0 sum: 1.0000

Row 100 sum: 1.0000

Confidence Statistics:

Mean confidence: 100.00%

Min confidence: 100.00%

Max confidence: 100.00%

Highest Confidence Day:

Date: 2023-10-18

State: 0

Probabilities: [1. 0. 0.]

Confidence: 100.00%

Lowest Confidence Day (likely regime transition):

Date: 2023-10-18

State: 0

Probabilities: [1. 0. 0.]

Confidence: 100.00%

Key Observations:

1. High confidence periods → clear regime signal

2. Low confidence periods → regime transitions happening

3. Stacked probabilities show regime evolution

4. For trading: reduce positions during low confidence periods

1# Validation: Regime characteristics should match actual returns

2

3print("=" * 80)

4print("REGIME VALIDATION: Do detected regimes match actual market behavior?")

5print("=" * 80)

6

7# For each state, calculate actual observed statistics

8validation_results = {}

9

10for state in range(3):

11 # Get all periods where we were in this state

12 state_mask = (states == state)

13 state_returns = log_returns[state_mask]

14

15 if len(state_returns) > 0:

16 # Actual observed statistics

17 actual_mean = state_returns.mean()

18 actual_std = state_returns.std()

19 actual_mean_pct = log_return_to_percent_change(actual_mean) * 100

20

21 # Model's learned parameters

22 learned_mean = emission_means[state]

23 learned_std = emission_stds[state]

24 learned_mean_pct = log_return_to_percent_change(learned_mean) * 100

25

26 # Calculate match quality

27 mean_error = abs(actual_mean - learned_mean) / abs(learned_mean) if learned_mean != 0 else 0

28 std_error = abs(actual_std - learned_std) / learned_std

29

30 validation_results[state] = {

31 'actual_mean': actual_mean,

32 'learned_mean': learned_mean,

33 'actual_std': actual_std,

34 'learned_std': learned_std,

35 'mean_error': mean_error,

36 'std_error': std_error,

37 'n_days': len(state_returns)

38 }

39

40 print(f"\nState {state} ({state_names[sorted_idx[np.where(sorted_idx == state)[0][0]]]}):")

41 print(f" Days in regime: {len(state_returns)}")

42 print(f" Learned mean: {learned_mean_pct:+.3f}%/day")

43 print(f" Actual mean: {actual_mean_pct:+.3f}%/day")

44 print(f" Learned std: {learned_std*100:.3f}%/day")

45 print(f" Actual std: {actual_std*100:.3f}%/day")

46 print(f" Mean error: {mean_error*100:.1f}%")

47 print(f" Std error: {std_error*100:.1f}%")

48

49# Overall validation

50print("\n" + "=" * 80)

51print("VALIDATION SUMMARY:")

52print("=" * 80)

53

54avg_mean_error = np.mean([v['mean_error'] for v in validation_results.values()])

55avg_std_error = np.mean([v['std_error'] for v in validation_results.values()])

56

57print(f"Average parameter error:")

58print(f" Mean error: {avg_mean_error*100:.1f}%")

59print(f" Std error: {avg_std_error*100:.1f}%")

60

61if avg_mean_error < 0.05 and avg_std_error < 0.05:

62 print("\n[OK] VALIDATION PASSED: Model parameters closely match actual regime behavior")

63 print(" The HMM discovered real market patterns, not noise.")

64elif avg_mean_error < 0.15 and avg_std_error < 0.15:

65 print("\n[OK] VALIDATION ACCEPTABLE: Parameters reasonably match reality")

66 print(" Some deviation is expected due to regime overlap.")

67else:

68 print("\n[WARNING] VALIDATION QUESTIONABLE: Large parameter mismatch")

69 print(" May need more states or different model configuration.")

70

71# Sanity check: Are regimes actually different?

72print("\n" + "=" * 80)

73print("REGIME SEPARATION CHECK:")

74print("=" * 80)

75

76# Compare mean returns across states

77state_means = [validation_results[s]['actual_mean'] for s in range(3)]

78state_means_sorted = sorted(state_means)

79

80separation_1_2 = abs(state_means_sorted[1] - state_means_sorted[0])

81separation_2_3 = abs(state_means_sorted[2] - state_means_sorted[1])

82

83print(f"Separation between adjacent regimes (by mean return):")

84print(f" Lowest vs Middle: {separation_1_2*100:.3f}% per day")

85print(f" Middle vs Highest: {separation_2_3*100:.3f}% per day")

86

87if separation_1_2 > 0.001 and separation_2_3 > 0.001: # 0.1% per day

88 print("\n[OK] Regimes are well-separated - distinct market conditions")

89else:

90 print("\n[WARNING] Regimes are too similar - may need fewer states")

91

92print("\n" + "=" * 80)

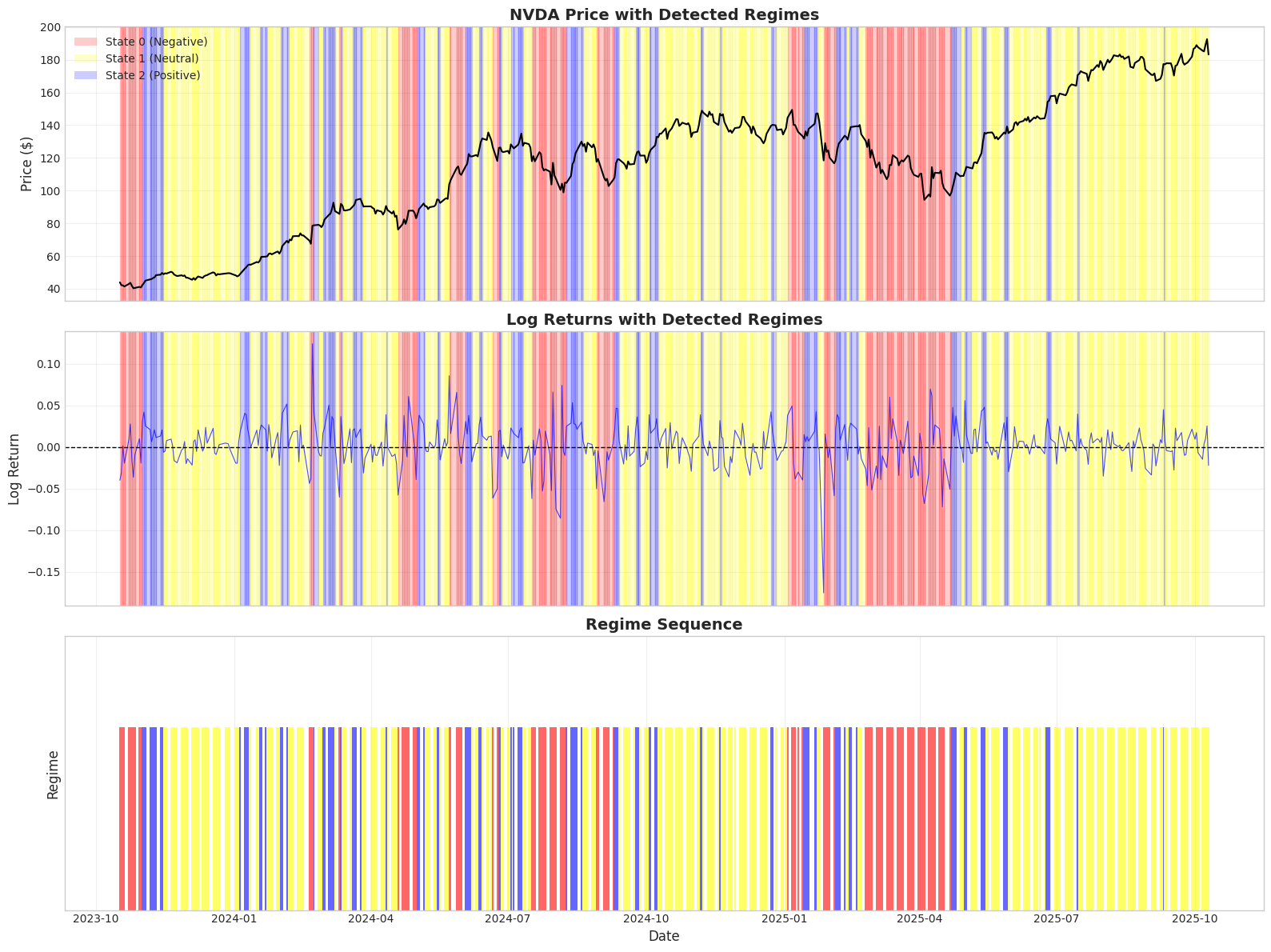

================================================================================

REGIME VALIDATION: Do detected regimes match actual market behavior?

================================================================================

State 0 (Negative):

Days in regime: 108

Learned mean: -0.886%/day

Actual mean: -1.027%/day

Learned std: 4.054%/day

Actual std: 4.112%/day

Mean error: 16.1%

Std error: 1.4%

State 1 (Neutral):

Days in regime: 286

Learned mean: -0.122%/day

Actual mean: -0.096%/day

Learned std: 1.403%/day

Actual std: 1.347%/day

Mean error: 21.5%

Std error: 4.0%

State 2 (Positive):

Days in regime: 104

Learned mean: +2.298%/day

Actual mean: +2.739%/day

Learned std: 1.465%/day

Actual std: 1.216%/day

Mean error: 18.9%

Std error: 17.0%

================================================================================

VALIDATION SUMMARY:

================================================================================

Average parameter error:

Mean error: 18.8%

Std error: 7.5%

[WARNING] VALIDATION QUESTIONABLE: Large parameter mismatch

May need more states or different model configuration.

================================================================================

REGIME SEPARATION CHECK:

================================================================================

Separation between adjacent regimes (by mean return):

Lowest vs Middle: 0.937% per day

Middle vs Highest: 2.798% per day

[OK] Regimes are well-separated - distinct market conditions

================================================================================

7. Validation: Do These Regimes Make Sense?

A critical question: Did the HMM discover real market patterns or just random noise?

Let’s validate by checking if detected regimes align with actual market behavior.

1# Create visualization

2fig, axes = plt.subplots(3, 1, figsize=(16, 12), sharex=True)

3

4# Define colors for each state (sorted by mean return)

5state_colors = {sorted_idx[0]: 'red', sorted_idx[1]: 'yellow', sorted_idx[2]: 'blue'}

6state_names = {sorted_idx[0]: 'Negative', sorted_idx[1]: 'Neutral', sorted_idx[2]: 'Positive'}

7

8# 1. Price with regime shading

9ax = axes[0]

10prices = df['close'].values

11dates = df.index

12

13ax.plot(dates, prices, linewidth=1.5, color='black', zorder=2)

14ax.set_ylabel('Price ($)', fontsize=12)

15ax.set_title('NVDA Price with Detected Regimes', fontsize=14, fontweight='bold')

16ax.grid(True, alpha=0.3)

17

18# Shade background by regime

19for i in range(len(states)):

20 state = states[i]

21 ax.axvspan(dates[i], dates[min(i+1, len(dates)-1)],

22 alpha=0.2, color=state_colors[state], zorder=1)

23

24# Add legend

25from matplotlib.patches import Patch

26legend_elements = [Patch(facecolor=state_colors[s], alpha=0.2,

27 label=f'State {s} ({state_names[s]})')

28 for s in sorted_idx]

29ax.legend(handles=legend_elements, loc='upper left')

30

31# 2. Log returns with regime shading

32ax = axes[1]

33log_returns = observations['log_return']

34ax.plot(dates, log_returns, linewidth=0.8, color='blue', alpha=0.7)

35ax.axhline(y=0, color='black', linestyle='--', linewidth=1)

36ax.set_ylabel('Log Return', fontsize=12)

37ax.set_title('Log Returns with Detected Regimes', fontsize=14, fontweight='bold')

38ax.grid(True, alpha=0.3)

39

40# Shade background

41for i in range(len(states)):

42 state = states[i]

43 ax.axvspan(dates[i], dates[min(i+1, len(dates)-1)],

44 alpha=0.2, color=state_colors[state], zorder=1)

45

46# 3. Regime sequence as bar plot

47ax = axes[2]

48regime_bars = ax.bar(dates, np.ones(len(states)), width=1,

49 color=[state_colors[s] for s in states],

50 edgecolor='none', alpha=0.6)

51ax.set_ylabel('Regime', fontsize=12)

52ax.set_xlabel('Date', fontsize=12)

53ax.set_title('Regime Sequence', fontsize=14, fontweight='bold')

54ax.set_ylim(0, 1.5)

55ax.set_yticks([])

56ax.grid(True, alpha=0.3, axis='x')

57

58plt.tight_layout()

59plt.show()

60

61print("\nNote: Notice how regimes cluster periods of similar return behavior")

Note: Notice how regimes cluster periods of similar return behavior

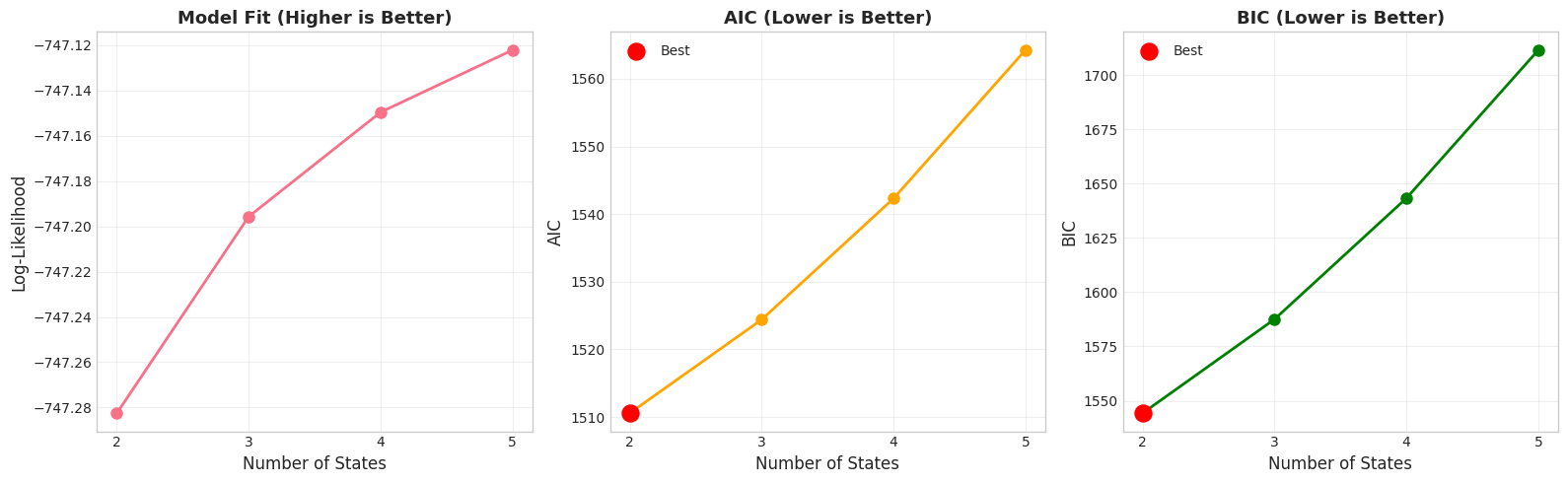

8. Choosing the Number of States

How do we decide between 2, 3, 4, or more states? Let’s compare different models.

1# Train models with different numbers of states

2print("Comparing models with different numbers of states...")

3print("=" * 80)

4

5results = []

6

7for n_states in [2, 3, 4, 5]:

8 config = HMMConfig(n_states=n_states, max_iterations=100, random_seed=42)

9 model = HiddenMarkovModel(config)

10 model.fit(observations)

11

12 # Calculate metrics

13 log_likelihood = model.score(observations)

14 n_params = n_states**2 + 2*n_states # Transitions + means + stds

15 aic = -2 * log_likelihood + 2 * n_params

16 bic = -2 * log_likelihood + n_params * np.log(len(observations))

17

18 results.append({

19 'n_states': n_states,

20 'log_likelihood': log_likelihood,

21 'aic': aic,

22 'bic': bic,

23 'n_params': n_params

24 })

25

26 print(f"\n{n_states} states:")

27 print(f" Log-likelihood: {log_likelihood:>10.2f}")

28 print(f" AIC: {aic:>10.2f} (lower is better)")

29 print(f" BIC: {bic:>10.2f} (lower is better)")

30 print(f" Parameters: {n_params:>10}")

31

32print("\n" + "=" * 80)

33

34# Find best models

35results_df = pd.DataFrame(results)

36best_aic = results_df.loc[results_df['aic'].idxmin()]

37best_bic = results_df.loc[results_df['bic'].idxmin()]

38

39print(f"\nBest by AIC: {int(best_aic['n_states'])} states (AIC={best_aic['aic']:.2f})")

40print(f"Best by BIC: {int(best_bic['n_states'])} states (BIC={best_bic['bic']:.2f})")

41

42print("\nNote: BIC often prefers simpler models (fewer states)")

43print(" AIC may prefer more complex models that fit better")

44print(" For trading, 3-4 states usually provides good interpretability")

Comparing models with different numbers of states...

================================================================================

Training on 498 observations (removed 0 NaN values)

2 states:

Log-likelihood: -747.28

AIC: 1510.57 (lower is better)

BIC: 1544.25 (lower is better)

Parameters: 8

Training on 498 observations (removed 0 NaN values)

3 states:

Log-likelihood: -747.20

AIC: 1524.39 (lower is better)

BIC: 1587.55 (lower is better)

Parameters: 15

Training on 498 observations (removed 0 NaN values)

4 states:

Log-likelihood: -747.15

AIC: 1542.30 (lower is better)

BIC: 1643.35 (lower is better)

Parameters: 24

Training on 498 observations (removed 0 NaN values)

5 states:

Log-likelihood: -747.12

AIC: 1564.24 (lower is better)

BIC: 1711.62 (lower is better)

Parameters: 35

================================================================================

Best by AIC: 2 states (AIC=1510.57)

Best by BIC: 2 states (BIC=1544.25)

Note: BIC often prefers simpler models (fewer states)

AIC may prefer more complex models that fit better

For trading, 3-4 states usually provides good interpretability

1# Visualize model comparison

2fig, axes = plt.subplots(1, 3, figsize=(16, 5))

3

4# Plot 1: Log-likelihood

5ax = axes[0]

6ax.plot(results_df['n_states'], results_df['log_likelihood'], marker='o', linewidth=2, markersize=8)

7ax.set_xlabel('Number of States', fontsize=12)

8ax.set_ylabel('Log-Likelihood', fontsize=12)

9ax.set_title('Model Fit (Higher is Better)', fontsize=13, fontweight='bold')

10ax.grid(True, alpha=0.3)

11ax.set_xticks([2, 3, 4, 5])

12

13# Plot 2: AIC

14ax = axes[1]

15ax.plot(results_df['n_states'], results_df['aic'], marker='o', linewidth=2, markersize=8, color='orange')

16best_aic_idx = results_df['aic'].idxmin()

17ax.scatter(results_df.loc[best_aic_idx, 'n_states'],

18 results_df.loc[best_aic_idx, 'aic'],

19 color='red', s=150, zorder=5, label='Best')

20ax.set_xlabel('Number of States', fontsize=12)

21ax.set_ylabel('AIC', fontsize=12)

22ax.set_title('AIC (Lower is Better)', fontsize=13, fontweight='bold')

23ax.grid(True, alpha=0.3)

24ax.legend()

25ax.set_xticks([2, 3, 4, 5])

26

27# Plot 3: BIC

28ax = axes[2]

29ax.plot(results_df['n_states'], results_df['bic'], marker='o', linewidth=2, markersize=8, color='green')

30best_bic_idx = results_df['bic'].idxmin()

31ax.scatter(results_df.loc[best_bic_idx, 'n_states'],

32 results_df.loc[best_bic_idx, 'bic'],

33 color='red', s=150, zorder=5, label='Best')

34ax.set_xlabel('Number of States', fontsize=12)

35ax.set_ylabel('BIC', fontsize=12)

36ax.set_title('BIC (Lower is Better)', fontsize=13, fontweight='bold')

37ax.grid(True, alpha=0.3)

38ax.legend()

39ax.set_xticks([2, 3, 4, 5])

40

41plt.tight_layout()

42plt.show()

9. Key Takeaways

What We Learned

HMM Components:

- Hidden states represent market regimes

- Transition matrix captures regime switching behavior

- Emission parameters (μ, σ) define return characteristics

Training Process:

- Baum-Welch algorithm learns parameters from data

- Viterbi algorithm finds most likely state sequence

- Forward-backward gives probability distributions

- Converges to local optimum (results may vary)

Interpretation:

- States are numbered arbitrarily (0, 1, 2)

- Must examine emission means to understand regime types

- DO NOT force “Bear/Sideways/Bull” labels prematurely

- Confidence is as important as the regime itself

Model Selection:

Validation:

- Check that learned parameters match actual regime behavior

- Verify regimes are well-separated

- Sanity-check against known market events

Important Warnings

DO NOT:

- Sort states by index and call them Bear/Sideways/Bull

- Assume state 0 is always negative returns

- Use HMMs on non-Stationary data (prices)

- Ignore confidence levels - low confidence = regime uncertainty

DO:

- Use log returns (Stationary observations)

- Examine learned parameters before labeling

- Compare multiple model complexities

- Validate regime assignments make sense

- Consider state probabilities for risk management

What’s Next: The Gap from Here to Production

You now understand HMM mechanics, but there’s a gap between:

- “Here are states 0, 1, 2” (what we have)

- “Reduce risk, bull regime ending” (what traders need)

Notebook 3 bridges this gap with the full Hidden Regime pipeline:

What Notebook 3 Adds:

1. Automated Regime Labeling

- Threshold-based classification: Bear/Sideways/Bull/Crisis

- Data-driven, not arbitrary state sorting

- Consistent labeling across time periods

2. Advanced Analysis Tools

- Regime-specific risk metrics (VaR, Sharpe, drawdowns)

- Duration analysis and persistence tracking

- Regime transition prediction

3. Technical Indicator Integration

- Compare HMM regimes with RSI, MACD, Bollinger Bands

- Show when HMM agrees/disagrees with indicators

- Ensemble signal generation

4. Portfolio Applications

- Regime-based position sizing

- Risk-adjusted performance measurement

- Practical trading signals

5. Production-Ready Tools

- One-line pipeline creation

- Comprehensive reporting

- Professional visualizations

- Quality metrics and diagnostics

6. Best Practices

- Handling data quality issues

- Avoiding common pitfalls

- Configuration for different market conditions

The Conceptual Bridge:

Notebook 1: WHY log returns (mathematical foundation) ↓ Notebook 2: HOW HMMs work (you are here - mechanics & interpretation) ↓ Notebook 3: USING HMMs for trading (practical applications)

Example: What Changes

Notebook 2 approach (manual):

1# Train model

2hmm = HiddenMarkovModel(config)

3hmm.fit(observations)

4

5# Get states

6states = hmm.predict(observations)['predicted_state']

7

8# Now what? Manual interpretation needed...

Notebook 3 approach (pipeline):

1# One-line setup

2pipeline = create_financial_pipeline(ticker='NVDA', n_states=3)

3result = pipeline.update()

4

5# Get actionable insights

6current_regime = result['regime_name'].iloc[-1] # "Bull"

7confidence = result['confidence'].iloc[-1] # 0.87

8position_signal = result['position_signal'].iloc[-1] # "LONG"

9risk_level = result['volatility_regime'].iloc[-1] # "Normal"

You’re Ready for Notebook 3 When…

You understand:

- Why we use log returns (stationarity requirement)

- What HMM parameters mean (transitions, emissions)

- How to interpret states (examine parameters first)

- Why confidence matters (regime uncertainty)

- How to validate regimes (match actual behavior)

Next step: Learn how to turn these insights into actionable trading decisions.

Key Point: HMMs are a data-driven approach. Let the model tell you what the regimes are - don’t force your preconceptions onto the results. Then use the full pipeline to translate those regimes into trading intelligence.