Hidden Regime Pipeline

Hidden Regime Pipeline

From Manual HMM to Production-Ready Pipeline

See the Notebook source on GitHub.

Your Learning Journey So Far

Notebook 1: Why Use Log Returns?

You learned WHY we use log returns:

- ✓ Stationarity (required for HMMs)

- ✓ Time additivity (returns simply add)

- ✓ Scale invariance (compare $60 and $500 stocks)

- ✓ Symmetric treatment (gains/losses balanced)

- ✓ Cross-asset comparability

Key Takeaway: Log returns aren’t convention—they’re mathematical necessity.

Notebook 2: HMM Basics

You learned HOW HMMs work:

- ✓ Hidden states represent market regimes

- ✓ Transition matrices capture regime persistence

- ✓ Emission parameters (μ, σ) define regime characteristics

- ✓ Viterbi algorithm finds most likely state sequence

- ✓ Forward-backward gives probability distributions

Key Takeaway: Don’t force “Bear/Bull” labels—let data reveal regimes.

Notebook 3: Production Pipeline (This Notebook)

You’ll learn USING the pipeline for real analysis:

- ✓ One-line pipeline setup (production efficiency)

- ✓ Automated regime labeling (threshold-based logic)

- ✓ Regime characteristics and persistence

- ✓ Choosing optimal number of states

- ✓ Best practices for regime detection

Scope Note: This notebook focuses on regime detection. For trading applications (risk management, position sizing, backtesting), see Notebook 4.

What This Notebook Covers

Part 1: Quick Pipeline Setup (Sections 1-2)

Part 2: Understanding Regime Classification (Sections 3-4)

Part 3: Regime Duration & Persistence (Section 5)

Part 4: Visualization (Section 6)

Part 5: Model Selection (Section 7)

Part 6: Best Practices & Next Steps (Section 8)

1import sys

2from pathlib import Path

3import numpy as np

4import pandas as pd

5import matplotlib.pyplot as plt

6import seaborn as sns

7from datetime import datetime, timedelta

8import warnings

9warnings.filterwarnings('ignore')

10

11# Add parent to path

12sys.path.insert(0, str(Path().absolute().parent))

13

14# Import hidden_regime using the full API

15import hidden_regime as hr

16

17# Plotting

18plt.style.use('seaborn-v0_8-whitegrid')

19sns.set_palette(sns.color_palette())

20

21print("Imports complete")

22print(f"hidden-regime version: {hr.__version__}")

Imports complete

hidden-regime version: 1.0.0

1. Quick Start: Pipeline Factory

The library provides factory functions for quick pipeline creation.

1# Create a complete financial pipeline with one function call

2ticker = 'NVDA'

3n_states = 3

4

5pipeline = hr.create_financial_pipeline(

6 ticker=ticker,

7 n_states=n_states,

8 include_report=False # We'll do custom analysis

9)

10

11# Display pipeline components

12print(f"Pipeline created for {ticker} with {n_states} states")

13print(f" Data loader: {type(pipeline.data).__name__}")

14print(f" Observations: {type(pipeline.observation).__name__}")

15print(f" Model: {type(pipeline.model).__name__}")

16print(f" Analysis: {type(pipeline.analysis).__name__}")

Pipeline created for NVDA with 3 states

Data loader: FinancialDataLoader

Observations: FinancialObservationGenerator

Model: HiddenMarkovModel

Analysis: FinancialAnalysis

2. Run the Complete Pipeline

The pipeline.update() method executes all stages:

- Data loading: Downloads historical price data

- Observation generation: Computes log returns

- Model training: Fits HMM using Baum-Welch algorithm

- Analysis: Generates regime classifications and metrics

1# Execute pipeline

2report = pipeline.update()

3

4# Get analysis results

5result = pipeline.component_outputs['analysis']

6

7# Display summary

8print(f"Analysis complete: {result.shape[0]} days, {result.shape[1]} metrics")

9print(f"Date range: {result.index[0].date()} to {result.index[-1].date()}")

Training on 500 observations (removed 0 NaN values)

Analysis complete: 500 days, 37 metrics

Date range: 2023-10-17 to 2025-10-14

3. Threshold-Based Regime Mapping

How Regimes Are Classified

The library uses data-driven thresholds on emission means $\mu_k$:

$ \text{regime}_k = \begin{cases} \text{Bear} & \text{if } \mu_k < \theta_{\text{bear}} \\ \text{Bull} & \text{if } \mu_k > \theta_{\text{bull}} \\ \text{Sideways} & \text{otherwise} \end{cases} $

Where $\theta_{\text{bear}}$ and $\theta_{\text{bull}}$ are determined by:

- Historical return distributions

- Volatility-adjusted cutoffs

- Statistical significance tests

Key Point: We do NOT sort states by index and assign “State 0 = Bear, State 1 = Sideways, State 2 = Bull”. The data reveals the regime types.

1# Get raw data with log returns

2raw_data = pipeline.data.get_all_data()

3

4# Find log_return column (case-insensitive)

5log_return_col = None

6for col in raw_data.columns:

7 if col.lower() == 'log_return':

8 log_return_col = col

9 break

10

11# Prepare regime data for visualization

12regimes = result['regime_name'].unique()

13regime_stats = []

14

15for regime in sorted(regimes):

16 regime_data = result[result['regime_name'] == regime]

17 n_days = len(regime_data)

18 pct_time = n_days / len(result) * 100

19 state_num = regime_data['predicted_state'].iloc[0]

20

21 stats = {

22 'regime': regime,

23 'state': state_num,

24 'days': n_days,

25 'pct_time': pct_time

26 }

27

28 # Get log returns for this regime by aligning indices

29 if log_return_col is not None:

30 regime_indices = regime_data.index

31 obs_returns = raw_data.loc[regime_indices, log_return_col].dropna()

32

33 if len(obs_returns) > 0:

34 avg_log = obs_returns.mean()

35 avg_pct = hr.log_return_to_percent_change(avg_log) * 100

36 vol_daily = obs_returns.std() * 100

37 vol_annual = vol_daily * np.sqrt(252)

38

39 stats.update({

40 'daily_return': avg_pct,

41 'daily_vol': vol_daily,

42 'annual_return': avg_pct * 252,

43 'annual_vol': vol_annual

44 })

45

46 regime_stats.append(stats)

47

48# Create visualization with larger figure size

49fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(18, 7))

50

51# Get regime colors

52unique_regimes = sorted(result['regime_name'].unique())

53from hidden_regime.visualization import get_regime_colors

54color_list = get_regime_colors(len(unique_regimes), color_scheme="colorblind_safe")

55regime_colors = dict(zip(unique_regimes, color_list))

56

57# Left: Pie chart of regime distribution

58sizes = [s['pct_time'] for s in regime_stats]

59labels = [f"{s['regime']}\n{s['pct_time']:.1f}%" for s in regime_stats]

60colors = [regime_colors[s['regime']] for s in regime_stats]

61

62wedges, texts, autotexts = ax1.pie(sizes, labels=labels, colors=colors, autopct='',

63 startangle=90, textprops={'fontsize': 13, 'fontweight': 'bold'})

64ax1.set_title('Regime Distribution\n(% of Time)', fontsize=15, fontweight='bold', pad=20)

65

66# Right: Bar chart of returns by regime

67regime_names = [s['regime'] for s in regime_stats]

68returns = [s.get('annual_return', 0) for s in regime_stats]

69bar_colors = [regime_colors[s['regime']] for s in regime_stats]

70

71bars = ax2.barh(regime_names, returns, color=bar_colors, alpha=0.7, edgecolor='black', linewidth=1.5)

72ax2.axvline(x=0, color='black', linestyle='-', linewidth=0.8)

73ax2.set_xlabel('Annualized Return (%)', fontsize=13)

74ax2.set_ylabel('Regime', fontsize=13)

75ax2.set_title('Expected Returns by Regime', fontsize=15, fontweight='bold', pad=20)

76ax2.grid(True, alpha=0.3, axis='x')

77ax2.tick_params(axis='both', labelsize=12)

78

79# Add value labels on bars

80for i, (bar, val) in enumerate(zip(bars, returns)):

81 if val != 0: # Only add label if we have data

82 label_x = val + (3 if val > 0 else -3)

83 ha = 'left' if val > 0 else 'right'

84 ax2.text(label_x, bar.get_y() + bar.get_height()/2,

85 f'{val:+.1f}%', ha=ha, va='center', fontweight='bold', fontsize=12)

86

87plt.tight_layout()

88plt.show()

89

90# Print detailed statistics

91print("\nDetailed Regime Characteristics")

92print("=" * 80)

93for s in regime_stats:

94 print(f"\n{s['regime']} (State {s['state']})")

95 print("-" * 80)

96 print(f" Frequency: {s['days']} days ({s['pct_time']:.1f}% of period)")

97 if 'daily_return' in s:

98 print(f" Daily: mu = {s['daily_return']:+.3f}% sigma = {s['daily_vol']:.3f}%")

99 print(f" Annualized: mu = {s['annual_return']:+.1f}% sigma = {s['annual_vol']:.1f}%")

100print("=" * 80)

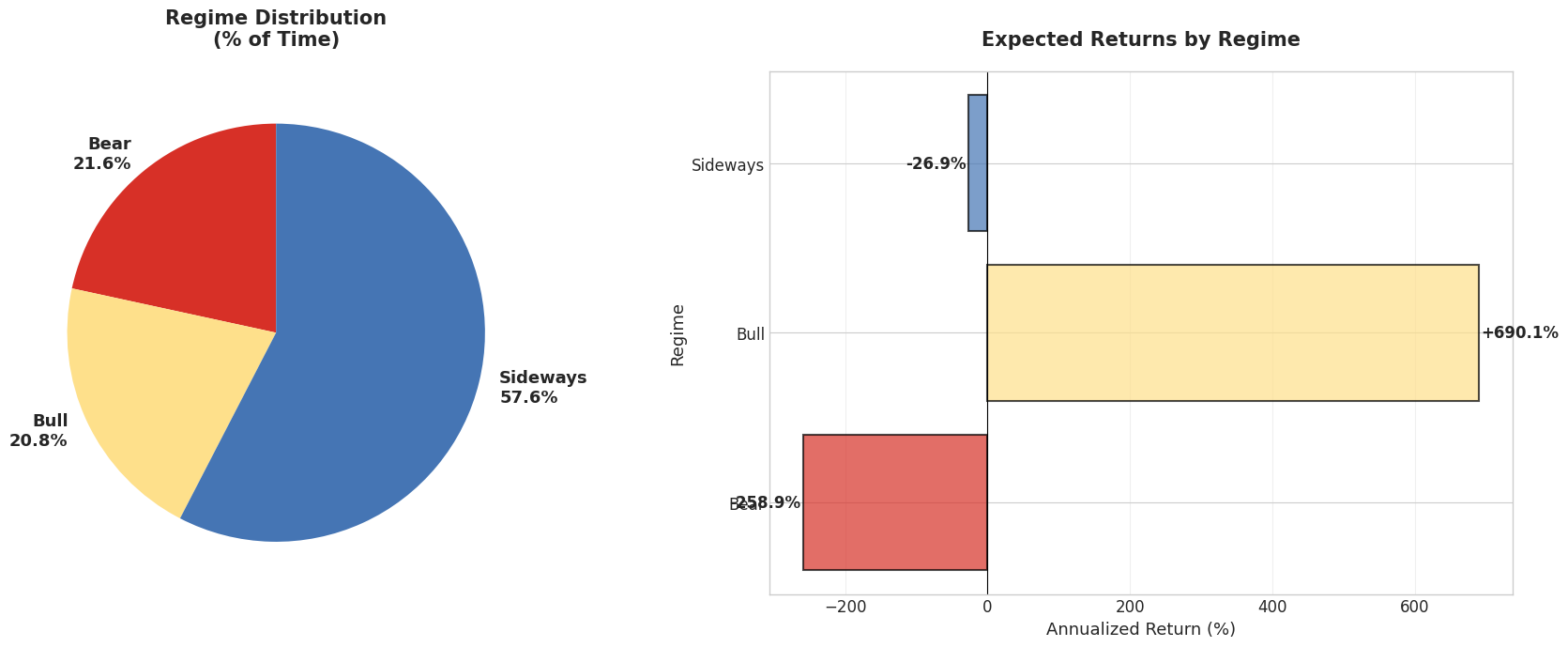

Detailed Regime Characteristics

================================================================================

Bear (State 0)

--------------------------------------------------------------------------------

Frequency: 108 days (21.6% of period)

Daily: mu = -1.027% sigma = 4.131%

Annualized: mu = -258.9% sigma = 65.6%

Bull (State 2)

--------------------------------------------------------------------------------

Frequency: 104 days (20.8% of period)

Daily: mu = +2.739% sigma = 1.221%

Annualized: mu = +690.1% sigma = 19.4%

Sideways (State 1)

--------------------------------------------------------------------------------

Frequency: 288 days (57.6% of period)

Daily: mu = -0.107% sigma = 1.356%

Annualized: mu = -26.9% sigma = 21.5%

================================================================================

4. Current Regime Status

State Probability Distribution

The HMM provides full probability distribution at each time point:

$ P(\text{state}_k \mid O_1, \ldots, O_T) = \frac{\alpha_T(k) \beta_T(k)}{\sum_{j} \alpha_T(j) \beta_T(j)} $

Where:

- $\alpha_t(k)$: Forward probability (probability of observations up to $t$ AND being in state $k$)

- $\beta_t(k)$: Backward probability (probability of future observations GIVEN state $k$ at $t$)

Confidence is the maximum probability: $\max_k P(\text{state}_k \mid \text{all data})$

1# Analyze current regime

2current = result.iloc[-1]

3current_regime = current['regime_name']

4

5# Count consecutive days in regime

6days_in_regime = 1

7for i in range(len(result)-2, -1, -1):

8 if result.iloc[i]['regime_name'] == current_regime:

9 days_in_regime += 1

10 else:

11 break

12

13# Get state probabilities

14state_probs = []

15state_names = []

16for state in range(n_states):

17 col_name = f'state_{state}_prob'

18 if col_name in result.columns:

19 prob = current[col_name]

20 # Find regime name for this state

21 state_regime = result[result['predicted_state'] == state]['regime_name'].iloc[0] \

22 if len(result[result['predicted_state'] == state]) > 0 else f"State {state}"

23 state_probs.append(prob)

24 state_names.append(state_regime)

25

26# Create bar chart

27fig, ax = plt.subplots(figsize=(12, 5))

28

29# Get colors for bars

30unique_regimes = sorted(result['regime_name'].unique())

31from hidden_regime.visualization import get_regime_colors

32color_list = get_regime_colors(len(unique_regimes), color_scheme="colorblind_safe")

33regime_colors = dict(zip(unique_regimes, color_list))

34bar_colors = [regime_colors.get(name, 'gray') for name in state_names]

35

36# Create horizontal bar chart

37bars = ax.barh(state_names, state_probs, color=bar_colors, alpha=0.7, edgecolor='black', linewidth=2)

38

39# Highlight the current regime (max probability)

40max_idx = np.argmax(state_probs)

41bars[max_idx].set_alpha(1.0)

42bars[max_idx].set_linewidth(3)

43

44# Add percentage labels

45for i, (bar, prob) in enumerate(zip(bars, state_probs)):

46 ax.text(prob + 0.02, bar.get_y() + bar.get_height()/2,

47 f'{prob*100:.1f}%', ha='left', va='center', fontweight='bold', fontsize=11)

48

49# Formatting

50ax.set_xlim(0, 1.1)

51ax.set_xlabel('Probability', fontsize=12)

52ax.set_title(f'Current Market Regime: {current_regime} ' +

53 f'(Confidence: {current["confidence"]*100:.1f}%)',

54 fontsize=14, fontweight='bold', pad=15)

55ax.grid(True, alpha=0.3, axis='x')

56

57# Add vertical line at confidence threshold

58ax.axvline(x=0.8, color='green', linestyle='--', alpha=0.5, linewidth=2, label='High confidence (>80%)')

59ax.legend(loc='lower right')

60

61plt.tight_layout()

62plt.show()

63

64# Print summary

65print(f"\nCurrent Market Status")

66print("=" * 70)

67print(f" Date: {result.index[-1].date()}")

68print(f" Regime: {current_regime}")

69print(f" Confidence: {current['confidence']*100:.1f}%")

70print(f" Duration: {days_in_regime} days in current regime")

71print("=" * 70)

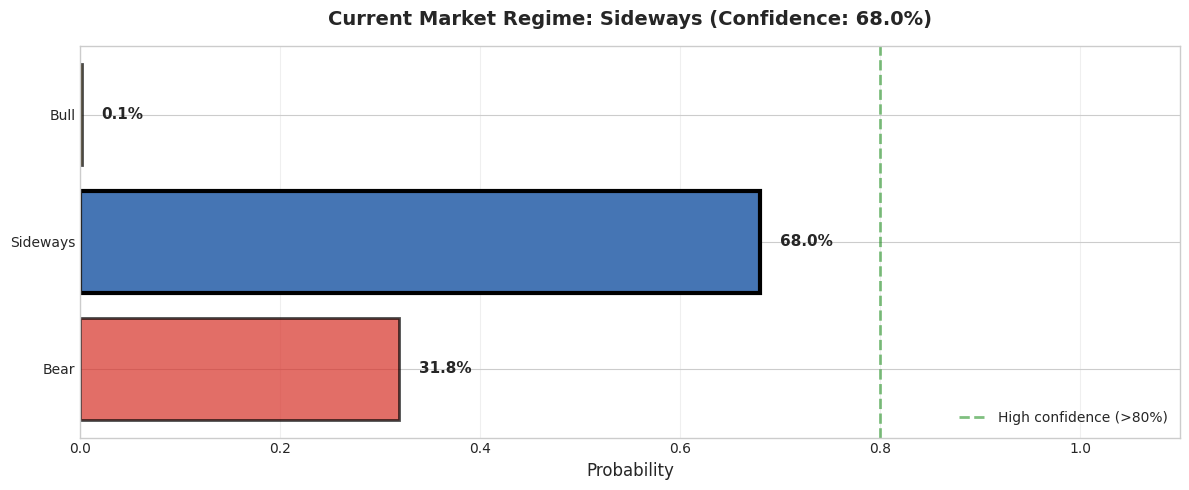

Current Market Status

======================================================================

Date: 2025-10-14

Regime: Sideways

Confidence: 68.0%

Duration: 24 days in current regime

======================================================================

5. Regime Duration Analysis

Expected Regime Duration

From the HMM transition matrix $\mathbf{A}$, the expected duration in regime $k$ is:

$ E[\tau_k] = \frac{1}{1 - A_{kk}} $

Where $A_{kk} = P(\text{state}_{t+1} = k \mid \text{state}_t = k)$ is the probability of staying in the same regime.

Example: If $A_{kk} = 0.90$, then $E[\tau] = \frac{1}{1-0.90} = 10$ days.

Why Duration Matters

- Short regimes (1-3 days): Possible overfitting or high-frequency market noise

- Medium regimes (5-15 days): Typical market regime persistence

- Long regimes (20+ days): Strong, stable market conditions

Duration analysis validates that the HMM is finding real market patterns, not random noise.

1# Calculate regime durations

2def calculate_regime_durations(df):

3 """Calculate duration of each regime period"""

4 durations = []

5 current_regime = df.iloc[0]['regime_name']

6 current_duration = 1

7

8 for i in range(1, len(df)):

9 if df.iloc[i]['regime_name'] == current_regime:

10 current_duration += 1

11 else:

12 durations.append({

13 'regime': current_regime,

14 'duration': current_duration,

15 'start': df.index[i-current_duration],

16 'end': df.index[i-1]

17 })

18 current_regime = df.iloc[i]['regime_name']

19 current_duration = 1

20

21 # Add final period

22 durations.append({

23 'regime': current_regime,

24 'duration': current_duration,

25 'start': df.index[len(df)-current_duration],

26 'end': df.index[-1]

27 })

28

29 return pd.DataFrame(durations)

30

31durations_df = calculate_regime_durations(result)

32

33# Display statistics

34print("Regime Duration Statistics")

35print("=" * 70)

36print(f"Total regime transitions: {len(durations_df)}\n")

37

38for regime in sorted(durations_df['regime'].unique()):

39 regime_durs = durations_df[durations_df['regime'] == regime]['duration']

40

41 print(f"{regime}:")

42 print(f" Occurrences: {len(regime_durs)} periods")

43 print(f" Average: {regime_durs.mean():.1f} days (median: {regime_durs.median():.0f})")

44 print(f" Range: {regime_durs.min()} - {regime_durs.max()} days")

45 print()

46

47# Show longest periods

48print("Longest Regime Periods:")

49print("-" * 70)

50longest = durations_df.nlargest(5, 'duration')

51for idx, row in longest.iterrows():

52 print(f" {row['regime']:<12} {row['duration']:>3} days " +

53 f"({row['start'].date()} → {row['end'].date()})")

54print("=" * 70)

Regime Duration Statistics

======================================================================

Total regime transitions: 75

Bear:

Occurrences: 11 periods

Average: 9.8 days (median: 6)

Range: 1 - 40 days

Bull:

Occurrences: 32 periods

Average: 3.2 days (median: 3)

Range: 1 - 10 days

Sideways:

Occurrences: 32 periods

Average: 9.0 days (median: 5)

Range: 1 - 39 days

Longest Regime Periods:

----------------------------------------------------------------------

Bear 40 days (2025-02-24 → 2025-04-21)

Sideways 39 days (2025-07-16 → 2025-09-09)

Sideways 34 days (2023-11-15 → 2024-01-04)

Sideways 24 days (2025-09-11 → 2025-10-14)

Sideways 22 days (2024-11-20 → 2024-12-20)

======================================================================

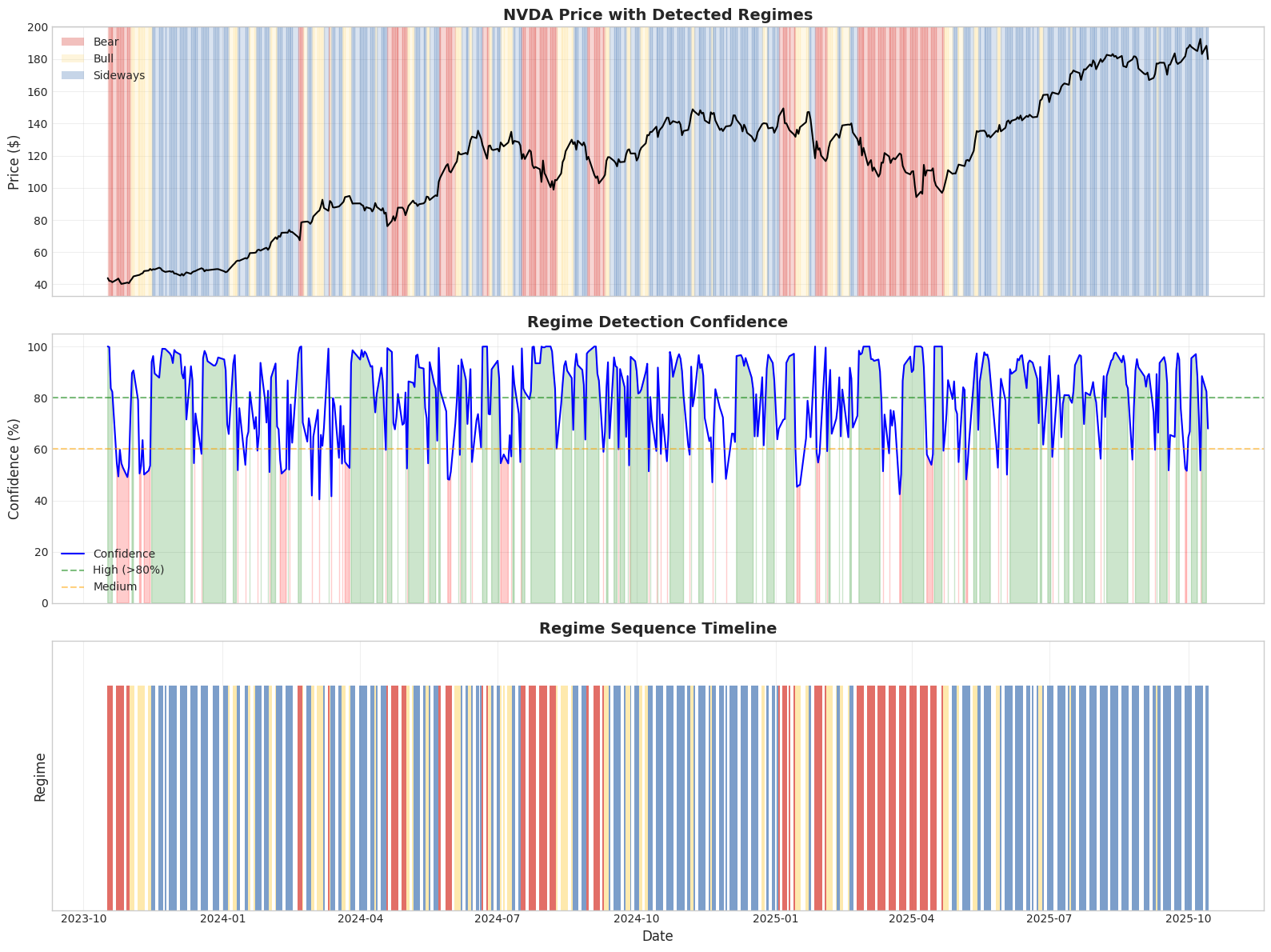

6. Visualization

Three-panel visualization showing:

- Price with regime shading: Visual alignment of regimes with price action

- Confidence levels: How certain the model is about each regime

- Regime timeline: Sequential regime transitions

1# Create regime visualization

2fig, axes = plt.subplots(3, 1, figsize=(16, 12), sharex=True)

3

4# Get raw price data

5raw_data = pipeline.data.get_all_data()

6close_col = next((col for col in raw_data.columns if col.lower() == 'close'), None)

7

8if close_col is None:

9 raise ValueError("Could not find 'close' column in data")

10

11# Get regime colors

12unique_regimes = sorted(result['regime_name'].unique())

13from hidden_regime.visualization import get_regime_colors

14color_list = get_regime_colors(len(unique_regimes), color_scheme="colorblind_safe")

15regime_colors = dict(zip(unique_regimes, color_list))

16

17# Panel 1: Price with regime shading

18ax = axes[0]

19ax.plot(raw_data.index, raw_data[close_col], linewidth=1.5, color='black', zorder=2)

20ax.set_ylabel('Price ($)', fontsize=12)

21ax.set_title(f'{ticker} Price with Detected Regimes', fontsize=14, fontweight='bold')

22ax.grid(True, alpha=0.3)

23

24# Shade background by regime

25for i in range(len(result)):

26 regime = result.iloc[i]['regime_name']

27 color = regime_colors.get(regime, 'gray')

28 ax.axvspan(result.index[i], result.index[min(i+1, len(result)-1)],

29 alpha=0.2, color=color, zorder=1)

30

31# Add legend

32from matplotlib.patches import Patch

33legend_elements = [Patch(facecolor=regime_colors.get(r, 'gray'), alpha=0.3, label=r)

34 for r in unique_regimes]

35ax.legend(handles=legend_elements, loc='upper left')

36

37# Panel 2: Confidence levels

38ax = axes[1]

39confidence_pct = result['confidence'] * 100

40

41ax.plot(result.index, confidence_pct, linewidth=1.5, color='blue', label='Confidence')

42ax.axhline(y=80, color='green', linestyle='--', alpha=0.5, label='High (>80%)')

43ax.axhline(y=60, color='orange', linestyle='--', alpha=0.5, label='Medium')

44

45# Shade confidence regions

46ax.fill_between(result.index, 0, confidence_pct,

47 where=(confidence_pct > 80), alpha=0.2, color='green')

48ax.fill_between(result.index, 0, confidence_pct,

49 where=(confidence_pct < 60), alpha=0.2, color='red')

50

51ax.set_ylabel('Confidence (%)', fontsize=12)

52ax.set_title('Regime Detection Confidence', fontsize=14, fontweight='bold')

53ax.grid(True, alpha=0.3)

54ax.legend(loc='lower left')

55ax.set_ylim(0, 105)

56

57# Panel 3: Regime timeline

58ax = axes[2]

59for i in range(len(result)):

60 regime = result.iloc[i]['regime_name']

61 color = regime_colors.get(regime, 'gray')

62 ax.bar(result.index[i], 1, width=1, color=color, edgecolor='none', alpha=0.7)

63

64ax.set_ylabel('Regime', fontsize=12)

65ax.set_xlabel('Date', fontsize=12)

66ax.set_title('Regime Sequence Timeline', fontsize=14, fontweight='bold')

67ax.set_ylim(0, 1.2)

68ax.set_yticks([])

69ax.grid(True, alpha=0.3, axis='x')

70

71plt.tight_layout()

72plt.show()

7. Model Comparison

Selecting Optimal Number of States

Model complexity tradeoff:

- Too few states: Cannot capture market nuances

- Too many states: Overfitting, very short regimes

Validation metrics:

- Average duration: Should be 5+ days for meaningful regimes

- Confidence: Higher confidence indicates clearer regime separation

- Number of parameters: $n_{\text{params}} = n^2 + 2n$ for $n$ states

- Interpretability: Can you explain what each regime represents?

1# Compare models with different numbers of states

2comparison_results = []

3

4print("Training models with 2-5 states...\n")

5

6for n in [2, 3, 4, 5]:

7 print(f" {n} states... ", end='', flush=True)

8

9 test_pipeline = hr.create_financial_pipeline(

10 ticker=ticker,

11 n_states=n,

12 include_report=False

13 )

14

15 _ = test_pipeline.update()

16 test_result = test_pipeline.component_outputs['analysis']

17

18 # Calculate metrics

19 n_params = n**2 + 2*n # Transitions + emissions

20 n_obs = len(test_result)

21 switches = (test_result['predicted_state'].diff() != 0).sum()

22 avg_duration = n_obs / switches if switches > 0 else n_obs

23 avg_conf = test_result['confidence'].mean() * 100

24

25 comparison_results.append({

26 'States': n,

27 'Parameters': n_params,

28 'Switches': switches,

29 'Avg Duration': f"{avg_duration:.1f}",

30 'Avg Confidence': f"{avg_conf:.1f}%"

31 })

32

33 print("done")

34

35# Display comparison table

36comp_df = pd.DataFrame(comparison_results)

37print("\n" + "=" * 70)

38print("Model Comparison Results")

39print("=" * 70)

40print(comp_df.to_string(index=False))

41print("=" * 70)

Training models with 2-5 states...

2 states... Training on 500 observations (removed 0 NaN values)

done

3 states... Training on 500 observations (removed 0 NaN values)

done

4 states... Training on 500 observations (removed 0 NaN values)

done

5 states... Training on 500 observations (removed 0 NaN values)

done

======================================================================

Model Comparison Results

======================================================================

States Parameters Switches Avg Duration Avg Confidence

2 8 24 20.8 89.2%

3 15 75 6.7 79.5%

4 24 101 5.0 78.8%

5 35 114 4.4 78.7%

======================================================================

Selection Guidelines

Interpreting the results:

| States | Typical Use Case | Watch Out For |

|---|---|---|

| 2 | Simple bull/bear classification | May miss sideways markets |

| 3 | Bear/Sideways/Bull (recommended) | Good balance |

| 4 | Adding crisis or rally states | Check duration > 5 days |

| 5+ | Very granular regimes | Often overfits, short regimes |

Red flags:

- ⚠️ Average duration < 5 days → Likely overfitting

- ⚠️ Confidence < 60% → Poor regime separation

- ⚠️ Too many switches → Capturing noise, not signal

Recommended: Start with 3 states. Add more only if:

- Durations remain meaningful (>5 days)

- Each regime has clear interpretation

- Validation on out-of-sample data shows improvement

7. Model Comparison

Compare different numbers of states to find the optimal model complexity.

8. Best Practices for Regime Detection

✓ DO These Things

1. Always Use Log Returns

- Ensures stationarity (required for HMMs)

- Proper statistical properties

- Cross-asset comparability

2. Let Data Determine Regimes

- Use threshold-based classification

- Don’t force “Bear/Bull” labels by sorting state indices

- Examine emission parameters before labeling

3. Check Confidence Levels

- Low confidence → regime uncertainty or transitions

- High confidence → reliable regime signals

- Use confidence for position sizing

4. Validate Regime Duration

- Very short regimes (< 3 days) → possible overfitting

- Typical regimes (5-15 days) → reasonable persistence

- Long regimes (20+ days) → strong, stable conditions

5. Compare Multiple Models

- Try 2-5 states systematically

- Balance fit quality vs complexity

- Use validation metrics (duration, confidence)

6. Monitor Regime Changes

- Large parameter shifts → market structure changes

- Regime transition patterns → leading indicators

- Confidence drops → early warning signals

⚠️ DON’T Do These Things

1. Don’t Use Raw Prices

- Prices are non-stationary

- Violates HMM assumptions

- Produces invalid inferences

2. Don’t Force Regime Labels

- State 0 ≠ automatically “Bear”

- Let emission means determine regime types

- Thresholds should be data-driven

3. Don’t Ignore Low Confidence

- Low confidence carries information

- Often signals regime transitions

- Critical for risk management

4. Don’t Assume Stationarity

- Market regimes evolve over time

- Parameters change with market structure

- Regular retraining may be needed

5. Don’t Overtrain

- More states ≠ better model

- 5+ states often overfit

- Focus on interpretability

6. Don’t Use Single Random Seed

- HMMs have local optima

- Results can vary by initialization

- Consider multiple runs or robust initialization

Production Checklist

Before deploying for real trading decisions:

- Verified log returns are used (not prices or simple returns)

- Checked regime durations are reasonable (not too short)

- Validated confidence levels are meaningful

- Compared 2-5 states and selected optimal complexity

- Examined regime characteristics match market intuition

- Tested on out-of-sample data

- Established monitoring for regime changes

- Integrated with risk management system (see Notebook 4)

9. Conclusion & Next Steps

What You’ve Accomplished

Congratulations! You now have a complete understanding of regime detection using HMMs:

From Notebook 1 (Mathematical Foundation):

- ✓ Why log returns are mathematically necessary

- ✓ Stationarity, additivity, and scale invariance

- ✓ Properties required for statistical modeling

From Notebook 2 (HMM Mechanics):

- ✓ How HMMs represent market regimes

- ✓ What transition matrices and emissions mean

- ✓ Viterbi vs forward-backward algorithms

- ✓ Interpreting states without forcing labels

From Notebook 3 (Production Pipeline) - This Notebook:

- ✓ One-line pipeline setup

- ✓ Automated threshold-based regime classification

- ✓ Regime duration and persistence analysis

- ✓ Model selection (2-5 states comparison)

- ✓ Visualization and interpretation

- ✓ Best practices for production use

The Complete Learning Path

Notebook 1: Mathematical Foundation (WHY)

↓

Notebook 2: HMM Mechanics (HOW)

↓

Notebook 3: Production Pipeline (USING) ← You are here

↓

Notebook 4: Trading Applications (PROFITING) ← Next step

What’s Next: Notebook 4 - Advanced Trading Applications

You can now detect regimes. Notebook 4 teaches you how to USE them for trading:

Part A: Regime-Specific Risk Management

- VaR and Expected Shortfall by regime

- Maximum drawdown analysis

- Sharpe ratios and risk-adjusted returns

- Dynamic position sizing based on regime risk

Part B: Technical Indicator Integration

- Combining HMM regimes with RSI, MACD, Bollinger Bands

- Agreement/disagreement analysis

- When to trust HMMs vs indicators

- Ensemble signal generation

Part C: Portfolio Applications

- Position signals (LONG/SHORT/NEUTRAL)

- Confidence-weighted position sizing

- Signal strength methodology

- Risk-adjusted portfolio allocation

Part D: Backtesting & Validation

- Hypothetical performance comparison

- Walk-forward analysis

- Regime-based strategy testing

- Out-of-sample validation

Practical Next Steps

If you want to continue learning:

- Open Notebook 4 to learn trading applications

- Apply these techniques to your own tickers

- Experiment with different time periods

- Try different numbers of states

If you’re ready for production:

- Review the best practices checklist above

- Test on multiple assets and time periods

- Validate regime stability over time

- Integrate with your existing trading system

- Start with paper trading before real capital

If you want to customize:

- Modify threshold values for regime classification

- Add your own features beyond log returns

- Implement custom risk metrics

- Integrate with other analysis tools

Key Takeaways

Regime detection is a tool, not a crystal ball.

Use it to:

- Understand current market conditions

- Adjust risk based on regime characteristics

- Combine with other analysis methods

- Make more informed trading decisions

Don’t expect it to:

- Predict future price movements perfectly

- Work in all market conditions

- Replace fundamental analysis

- Guarantee profitable trades

Resources

- Documentation: Hidden Regime Docs

- Examples: More examples in

/examplesdirectory - Issues: Report bugs at GitHub

- Community: Share strategies and learn from others

Ready for trading applications? Open Notebook 4!